Starmageddon (or is it?) and a positive start to Q3

Author: Tom McGrath – Chief Investment Officer, 8AM Global

Market Review

The second quarter has started well for bonds and equities as investors regained the bullish disposition that has been in place for much of the year. There were meaningful gains all around; although the FTSE 100 lagged in relative terms with only a 0.5% increase, the more domestically focused FTSE 250 registered a 2.5% increase. The initial reaction of investors to a Labour government is positive. Bonds also enjoyed an excellent start as yields dropped in response to softening economic data, which also helped gold move toward its previous highs. Sterling also strengthened on the back of the election result.

UK – Starmageddon?

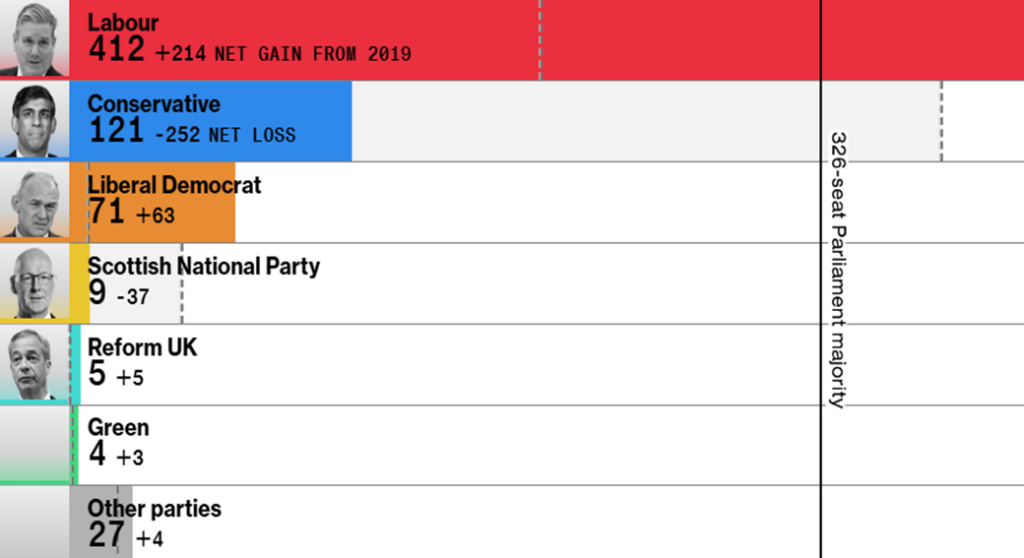

Keir Starmer’s Labour party achieved a landslide victory in the UK general election following the collapse of Rishi Sunak’s Conservatives, fundamentally altering the political landscape. Labour has secured 412 of the 650 seats in the House of Commons, the highest since Tony Blair’s 1997 victory. The Conservatives suffered their worst performance ever, winning just 121 seats, a loss of 252. Additionally, Nigel Farage’s populist Reform UK party captured substantial right-wing Conservative votes nationwide, although securing only 4 seats. The Liberal Democrats smashed down the ‘Blue Wall’ in the South, with more than 70 MPs.

UK equity investors have reasons to feel optimistic as Britain emerges as a stable entity in an otherwise volatile global political landscape. With US and European politics in disarray, the UK’s stability is appealing. With the election concluded and a substantial working majority for Labour, the new government will find they have inherited a reasonably solid economic position.

The separatist influence in Scotland has lessened, and the UK’s net trade post-Brexit is rebalancing positively, with the country recently surpassing France, the Netherlands, and Japan in total exports. The UK is out of recession, with a 0.7% quarter-on-quarter GDP growth in Q1 2024 and a promising outlook for the rest of the year. Real disposable incomes will rise by around 3% this year as inflation cools and recent tax cuts take effect. Some households and companies still hold substantial excess savings built up during the pandemic. As interest rates decrease, consumer spending and corporate investments are expected to increase, supporting GDP growth in 2025 and 2026.

Investor sentiment is bolstered by recent market activities, including 32 M&A transactions worth over £100 million in the first half of the year, with 60% involving foreign buyers at an average premium of 40%. This influx of foreign investment, along with attractive UK valuations and potential policy changes encouraging domestic investments, suggests that the UK equity market is a compelling prospect, arguably the most attractive on the world stage.

Historically, while Labour governments have had mixed impacts on the stock market, the current economic fundamentals and market conditions should be the primary focus for investors, not which party is in charge.

However, regardless of which party leads, there are still challenges ahead, such as net-zero commitments, productivity issues, and high national debt, that the new government will also need to address to sustain this positive momentum.

US Update

It was a shortened week of trading in the US, as Americans celebrated Independence Day on the 4th of July. Still, we got a very important economic update with the US Jobs report on Friday, which was likely just what the Fed wanted to see. US hiring and wage growth slowed in June, with the jobless rate reaching its highest level since late 2021, increasing the likelihood that the Federal Reserve will start cutting interest rates in the coming months. This potential change in the Federal Reserve’s interest rate decisions could have significant implications for the financial market.

Nonfarm payrolls rose by 206,000, while job growth for the previous two months was revised down by 111,000, according to the Bureau of Labor Statistics. It was stronger than the economists surveyed by Bloomberg had forecast (190,000) but arguably more importantly, the unemployment rate climbed to 4.1% as more individuals entered the labour force, and average hourly earnings moderated.

The average employment growth has cooled over the past three months, which aligns with other reports showing a sharp decline in job openings and an increase in unemployment benefit claims this year. Markets needed to determine what to make of the release, as the higher headline number differed from what investors expected. Still, the downward revisions to the previous two months combined with the rise in the unemployment rate were enough for them to conclude it was good news. The S&P 500 and the Nasdaq set all-time closing highs at the end of the week.

Biden refuses to go

The Democrat concern over Joe Biden’s disastrous televised debate with Donald Trump is growing, and there remains a possibility that he will be forced to step aside, with Kamala Harris, the current deputy, now emerging as the front runner. The President is having none of it, as he dismissed calls to end his re-election bid and denied that his debate performance wrought significant damage to his campaign. This defiant and incredulous posture looks increasingly likely to be challenged. In an ABC News interview, Biden refused to commit to an independent medical exam to reassure the public of his mental fitness, insisting he has the stamina to serve another four years. He declared that only the ‘Lord Almighty’ would prompt him to consider ending his bid. Don’t tempt fate was my takeaway from that!

Whether Biden’s strategy is determined or delusional, it remains the only viable option for a candidate seeking a second term. However, frustration is mounting within his party, and the issue will be put to the test in the coming week. News has surfaced about an unusual weekend meeting with top Democratic colleagues, possibly gathering to gauge the appetite for a leadership change ahead of a broader House Democratic caucus meeting early next week. The potential for a change in the Democratic party’s leadership is significant and would profoundly impact the upcoming election.

Vive Le France?

France goes back to the polls for the second round of elections, with voting again open for seats where the winner received less than 50% of the vote. There are still more than 500 districts up for grabs, and it now looks like Le Pen and her far-right National Rally party are set to fall well short of an absolute majority. The shortfall is due to political shenanigans and a broad ‘entente cordiale’ between Macron’s Centrist Alliance and the New Popular Front, which have strategically pulled over 200 candidates from ballots this week to avoid splitting opposition to the far right.

Regardless of the outcome of Sunday’s French parliamentary election, be prepared for increased volatility in the country’s stock and bond markets. The likely scenario of a gridlocked parliament could hinder France’s efforts to address its budget deficit and potentially stall President Emmanuel Macron’s pro-business reforms. This situation, however, is undoubtedly more desirable than the National Rally party gaining power with a clear majority.

This Week…

US earnings season kicks off with the big banks on Friday. Much now rests on the corporate sector to deliver strong growth, with estimates currently running at an 8.8% year-on-year increase for the S&P 500. We get the CPI Inflation data out of the US, Eurozone Industrial Production figures and a monthly estimate of UK GDP.

Important Information

This content is intended for financial professionals only. These are the author’s views at the time of writing and may be subject to change. This content is not intended to provide the basis for any investment advice or recommendation. Any forecasts, figures, opinions, tools, strategies, data, or investment techniques are included for information purposes only.

The information presented is considered to be accurate at the time of production and has been obtained from or based upon sources believed by the author to be reliable and accurate, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Please visit our Regulatory Information and Terms of Use pages for more information.

Production

Production