Back to flat for November

Author: Tom McGrath, CIO, 8AM Global Ltd

Market overview

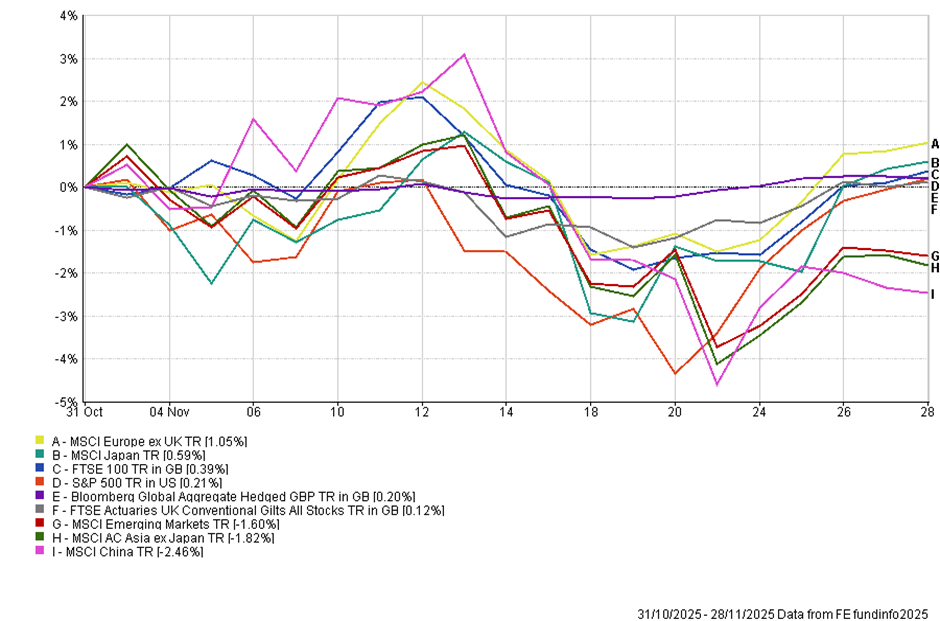

Markets have spent the past four weeks rotating, resetting, and occasionally jolting investors’ nerves but ultimately grinding their way back toward neutral. There was a degree of leadership reversal in November. This year’s winners: China, Asia ex-Japan and emerging markets, slipped a little, with China down more than 2% in November and EM/Asia ex-Japan both negative after a difficult mid-month drawdown. By contrast, Europe has quietly led developed markets, up just over 1% on the month. Japan has held its gains, supported by stimulus optimism and a softer yen. And the US, after its first meaningful 5% pullback since spring, has clawed back to flat line as a final score for November. So far, the global picture looks like broad but uneven stabilisation rather than a trend break.

The rebound last week helped. Both equities and bonds rallied globally, particularly small and mid-caps, as fading headwinds and improving liquidity gave markets breathing room. With the US government reopened, no further cash drain into the shutdown and AI earnings confirming that capex hasn’t overreached, sentiment finally stabilised. Rate-cut expectations for December have crept higher again, and with most 2025 earnings now reported and the news flow slowing into the holidays, markets have begun reassessing how much latent buying power remains. For now, markets sit in a surprisingly balanced place: not complacent, not fearful, just searching for direction. That, historically, is not the worst place to be.

UK – a budget that looked risky on paper but markets took in stride

Last week’s UK Budget was the biggest domestic story and, somewhat surprisingly, both gilts and UK equities handled it far better than many feared. Rachel Reeves delivered a package that avoided the expected income tax rise, kept policy modestly deflationary and, crucially, removed the final hurdle for the Bank of England to resume cutting interest rates as early as 18th December. For a market that has been craving clarity, that alone was enough to steady sentiment.

The Office for Budget Responsibility estimates that the rail fare freeze, an additional year of fuel duty relief, and measures to reduce household energy bills will lower CPI by around half a percentage point in the second quarter of next year. Together with the softer inflation data from October, this has allowed markets to price in almost a full chance of a cut next month, with around 60 to 65 basis points of total easing expected by the end of 2026.

The package’s structure doesn’t address any long-term issues. Reeves opted for a back-loaded consolidation, delaying the toughest tax rises until later in the decade and relying on a collection of smaller levies rather than one broad-based adjustment. The increase in the minimum wage and later changes to salary sacrifice rules will also push costs higher for some employers, even if these effects unfold slowly. Economists note that the budget helps near-term inflation but does not fully address the medium-term pressures from rising wage floors.

UK – Some positive fuel for the fire…

If there was a surprise last week, it was how calmly UK investment assets absorbed the Budget. Gilts tightened, sterling firmed, and UK financials actually led European peers higher. It was not the reaction many expected after weeks of gloomy commentary about Britain’s fiscal credibility. In fact, some of the more alarmist narratives look increasingly out of step with market reality. The political and economic challenges remain considerable, but from a market perspective, the Budget ended up soothing rather than unsettling investors, and it was interesting to see that small and mid-cap stocks led the charge higher last week.

A useful counterweight to overwhelming negativity came from Ambrose Evans Pritchard in The Telegraph, who argued that the story of a uniquely fragile UK is largely a self-inflicted myth. According to his piece, Britain remains a fiscal ‘saint’ compared with many major economies and is finally reversing decades of underinvestment in infrastructure, the real root of the productivity problem. He also notes that the UK is well positioned to benefit from the next wave of AI-driven productivity gains, with one of the world’s strongest AI sectors, Europe’s largest data-centre footprint, and the prospect of much more substantial trend growth over the next decade.

Regardless of whether one agrees with every part of the argument, it is a reminder that pessimism about the UK often overshoots. UK companies continue to deliver solid earnings, valuations remain among the cheapest in the developed world, and takeover activity shows no signs of slowing as global buyers keep taking advantage of the discount. Markets judged the Budget not as a threat to stability but as a modest, manageable event that leaves the BoE clear to resume cutting rates. That alone marks a shift in tone and helps explain why UK equities and gilts ended the week in better shape than many expected.

US – We might just get another Santa Rally

The US market spent last week unwinding the damage from the previous sell-off, with the S&P 500 recovering most of what it lost during the bitcoin-driven shakeout and the brief panic over an AI bubble. What looked like forced liquidation and margin calls in mid-November has eased, and once the pressure in crypto subsided, the equity market quickly stabilised. That pattern fits the view we highlighted previously: liquidity-driven pullbacks often burn out soon once the forced sellers are flushed through.

The AI narrative also swung back in a more constructive direction. While short-sellers continue to argue that hyperscaler accounting flatters margins and that rapid GPU cycles will crush returns, the market took comfort from Alphabet’s strong update on Gemini-3 and its ability to train large models on cheaper in-house chips. Nvidia itself has not bounced much, but the broader ecosystem has remained resilient, suggesting this is a debate about valuation and timing rather than a structural break in the AI investment cycle.

Technically, the S&P 500 moved back above its 50-day moving average and now sits within touching distance of the 7,000 level. A modest 2% gain would take it there. Fed communication helped, with New York Fed President John Williams signalling that another ‘adjustment’ to interest rates could come as soon as the 10th of December meeting. Markets interpreted that as a green light for an additional cut, reinforcing the sense that policy is shifting to a more accommodative stance as we head into year-end.

Sentiment has also reset in a healthier direction. A week ago, AAII readings and Fear & Greed indicators showed retail investors turning nervous, while institutional positioning data from Goldman and Deutsche Bank suggested professionals were underweight and cautious. That combination usually supports markets rather than undermines them. The heavy use of inverse ETFs and systematic de-risking into the mid-month drop also mirrors past tactical lows. None of this guarantees a smooth December, but it does remove some of the excess optimism that had built up through late October.

Leadership has broadened too. Last week’s rebound was driven not just by mega-caps but also by small-cap and mid-cap growth stocks, which benefited from lower rate expectations and better liquidity conditions. That broadening is welcome after months of very narrow US leadership. It does not rule out further bouts of volatility, particularly if crypto remains jumpy or investors continue to debate the sustainability of AI capex, but it does point to a market that still has enough underlying demand to absorb shocks.

Put together, the US picture remains one of resilience against an extremely noisy backdrop. Earnings momentum is still the anchor: forward S&P 500 earnings have risen about 30% since the cycle turned in October 2022, and dip-buying appetite remains surprisingly strong. The possibility of a Santa Rally is there, especially if liquidity stays supportive and the Fed delivers another cut. But the more pragmatic conclusion is simply this: the bull market looks intact, even if the path into year-end is likely to remain choppy.

China – Still the year’s outperformer, even after a soft patch

China gave back a little ground in November, slipping just over 2%, but the bigger picture remains far more encouraging than the month-to-month noise. Year-to-date, China is still the standout performer across global equities, up more than 32% and ahead of Asia ex-Japan, emerging markets and even the S&P 500. The latest data reinforced the sense of an economy cooling but not rolling over.

Weekend data showed that factory activity edged higher again in November, with the manufacturing PMI lifting to 49.2. It’s still technically in contraction, but the direction is gently improving, and some of the underlying details showed progress – better order books, stronger small-business activity, and continued growth in high-tech manufacturing. Services dipped after the earlier holiday boost washed through, but the softness looks more seasonal than structural.

The broader story hasn’t changed. Domestic demand is still rebuilding, the property drag hasn’t gone away, and the tariff overhang continues to weigh on sentiment. But the market is already looking past the bumps. Policy support is steady, earnings are stabilising, and the tech and innovation complex, which has driven much of China’s rally this year, remains in good health.

Unlike on previous occasions when the market has rallied strongly, it would seem that investors haven’t capitulated; if anything, positioning remains light and scepticism high. That combination leaves huge room for upside. With China still comfortably the best-performing major equity region this year, the recent consolidation feels like a breather.

Looking ahead – Data slowly returns, but visibility still limited

This week is the first real test of how markets cope as data flow begins to return after weeks of disruption. The shutdown and reporting delays mean investors are still operating with partial visibility, and the usual early-month rhythm won’t fully return. We won’t get a normal non-farm payrolls release, and the labour picture will instead be pieced together from whatever ancillary indicators come through. That alone keeps the potential for choppier swings in rates and the dollar.

In the US, the focus turns to the ISM surveys and weekly claims data, which will need to stand in for a full employment report. With the Fed now in blackout, the market will be left to interpret these numbers without any policy guidance, and that often produces sharper intraday moves than usual. China will release its trade figures, which should help clarify whether November’s softer PMIs were a one-off or the start of a more drawn-out cooling. Europe, meanwhile, offers final inflation prints and sentiment gauges that should confirm the disinflation trend and help anchor expectations for a prolonged ECB pause.

In the UK, attention stays on whether the post-Budget calm can hold. Housing and retail indicators will give an early read on consumer resilience heading into Christmas, and gilt markets will be watching closely to see if expectations for a December rate cut remain intact.

Overall, next week is less about blockbuster headlines and more about whether the returning data trickles reinforce the sense that the global backdrop has stabilised. After a month of noise and volatility, even modestly reassuring numbers would help keep the path open for a steadier run into year-end and possibly even lay the foundation for a Santa Rally…

This content is intended for financial professionals only. These are the author’s views at the time of writing and may be subject to change. This content is not intended to provide the basis for any investment advice or recommendation. Any forecasts, figures, opinions, tools, strategies, data, or investment techniques are included for information purposes only.

The information presented is considered to be accurate at the time of production and has been obtained from or based upon sources believed by the author to be reliable and accurate, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Please visit our Regulatory Information and Terms of Use pages for more information.

Production

Production