Settling in, not slowing down

Author: Tom McGrath, CIO, 8AM Global Ltd

As 2026 gets underway, financial markets are already beginning to find their rhythm. The opening days of the year delivered no shortage of headlines, from Venezuela to political noise out of Washington, yet the market response has been notably measured. Equity indices have held their ground, bond yields have edged lower, and volatility remains subdued. For all the background drama, this is starting to feel like a year that has begun with calm rather than panic.

The Venezuelan episode, while geopolitically significant, has so far failed to provoke any meaningful reaction in risk assets. Oil prices barely flinched, credit markets remained steady, and equities continued to grind higher. It may yet prove relevant from a supply-and-inflation perspective, but for now, it has been noted, digested, and largely ignored. Markets remain focused on fundamentals, growth, earnings and policy, rather than single-event geopolitics.

Across asset classes, the tone is one of digestion rather than exuberance. Equities enjoyed an early burst of optimism, particularly in Asia and emerging markets, but momentum has since cooled, with the US taking over as the primary driver of performance. Europe and the UK remain steady but unspectacular. Bond markets have been calm, yields drifting lower as investors price in slower growth and a more accommodative policy backdrop. There is no sense of stress in the system. If anything, the message is one of resilience.

UK

The FTSE 100 holding above the 10,000 level is symbolically important. It reinforces the idea that valuations and global earnings exposure continue to provide a solid floor for the market. The domestic backdrop remains softer. Christmas trading updates from the retail sector were mixed (at best) and, in some cases, outright disappointing. Tesco reported slower-than-expected festive sales, Associated British Foods issued a profit warning after weak Primark trading, and Greggs cited subdued confidence in the food-to-go market. Even Next, often an outlier, warned that growth is likely to slow as labour market pressure weighs on spending.

The message is familiar. Households remain cautious, confidence is fragile, and many consumers are still counting every penny. UK yields have edged lower, reflecting a market that is increasingly sceptical about growth and more comfortable with the idea of easier policy ahead. The FTSE’s resilience is therefore more a reflection of its global, defensive composition than any improvement in domestic fundamentals. This is a valuation and earnings story, not a domestic growth story.

US

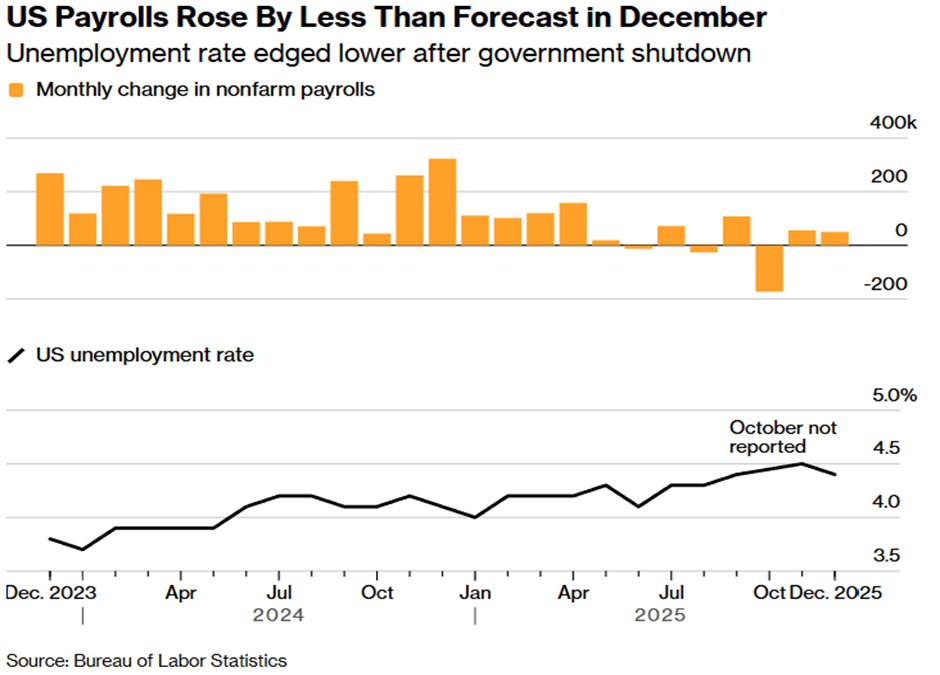

Market-wise, the focus is firmly on the US, where almost all the meaningful action is taking place. December’s employment report showed payrolls rising by just 50,000, below expectations and following downward revisions to the previous two months. It was one of the weakest years for hiring since 2009, and the data confirmed a year-long trend of cautious recruitment and limited layoffs. The unemployment rate edged down to 4.4%, but participation also dipped, and the number of long-term unemployed rose sharply over 2025.

On the surface, this points to a labour market that is cooling and increasingly fragile. Hiring is weak, job opportunities are limited, and pay gains are easing. Economists are warning that 2026 could be another challenging year for jobseekers, with affordability concerns likely to remain politically potent heading into the midterms. From a policy perspective, this backdrop explains why the Federal Reserve cut rates three times to close out 2025 and why investors continue to debate how much further easing might be required.

However, there is an important counterpoint, and it sits in the productivity data. US nonfarm business sector productivity surged by 4.9% in Q3 2025, following an upwardly revised 4.1% in Q2. Output growth has been strong, while hours worked have barely increased. Unit labour costs fell sharply in Q3 and are barely rising year on year. These are exceptional numbers, and they matter.

Productivity is the go-go juice for earnings. It allows the economy to grow without stoking inflation, supports margins and gives companies room to absorb costs without passing them straight on. It also creates space for central banks to ease policy without reigniting price pressures. In simple terms, the US is producing more with less, and that is precisely the kind of dynamic that underpins a more constructive view of the year ahead. It helps explain why equity markets have been so resilient in the face of slower hiring. The economy may be cooling at the margin, but it appears to be becoming more efficient.

There are early signs that this productivity story is being driven, at least in part, by the diffusion of AI and automation across the broader economy. While much of the focus over the past two years has been on the capital spending arms race among the large technology platforms, it may be the so-called “Impressive 493” that are now starting to see the real benefits. AI is gradually boosting efficiency, streamlining processes and lifting output across a wide range of sectors. This is a healthier, more sustainable story than one built purely on infrastructure spending and hype.

That context also helps frame the ongoing debate around the so-called AI bubble. Heavy investment, margin pressure and rising competition are likely to temper returns for the Magnificent Seven over time, but that does not mean a recession or a systemic shock. The air can come out of the AI capital-spending cycle without it bursting. If anything, it may simply mark a rotation of growth from the hyperscalers to the wider market as productivity gains spread.

The ‘Bubble’ even made the front cover of Bloomberg Business Week; typically, the cover stories seldom come to pass, so I take its feature as a positive contrarian indicator!

Stepping back and reading the tea leaves, the overall mood in markets is leaning toward optimism. However, there are still many ‘mean-reverters’ who believe equity markets are due for a correction this year after the strong gains of the last 3 years. We shall see; I fall into the optimist camp, although at the moment there is no sense of euphoria and still plenty of bears around to keep things balanced. That is a decent starting point for a year, especially as productivity improves and fiscal and monetary stimulus is expected.

This week…

Attention now turns to the corporate earnings season, which begins in earnest next week with the US banks. After a year dominated by macro narratives, policy shifts and AI speculation, this reporting season will offer a more grounded view of margins, demand and corporate confidence. Investors will be listening closely to commentary on loan growth, consumer behaviour, credit quality and capital spending intentions. In a market that has started the year calmly rather than frantically, earnings could be the next meaningful catalyst. If results and guidance reinforce the message of resilient growth, you can expect a lot more all-time highs set by the markets this year.

This content is intended for financial professionals only. These are the author’s views at the time of writing and may be subject to change. This content is not intended to provide the basis for any investment advice or recommendation. Any forecasts, figures, opinions, tools, strategies, data, or investment techniques are included for information purposes only.

The information presented is considered to be accurate at the time of production and has been obtained from or based upon sources believed by the author to be reliable and accurate, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Please visit our Regulatory Information and Terms of Use pages for more information.

Production

Production