Churn continues under the surface

Author: Tom McGrath, CIO, 8AM Global Ltd

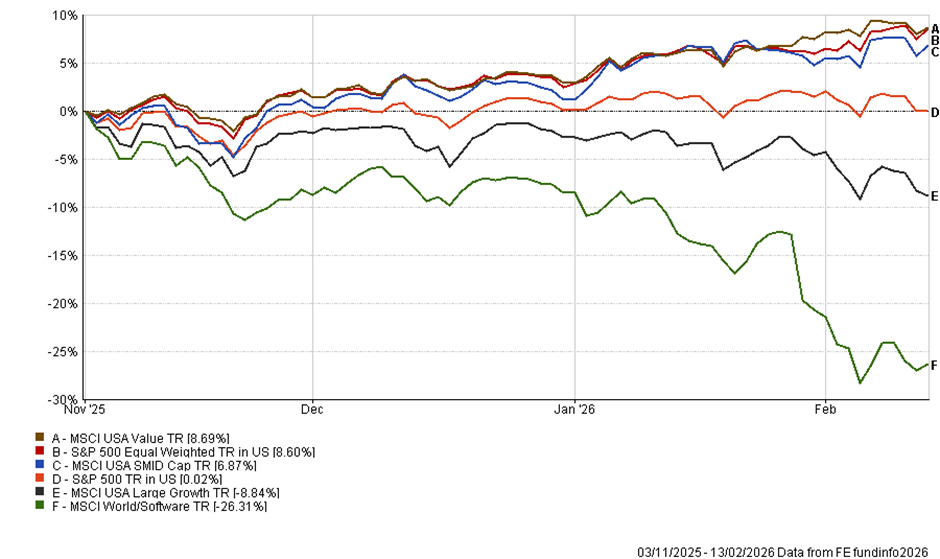

At a headline level, US equities have looked deceptively uneventful since early November. The S&P 500 is flat over that period. The chart below shows a market that has been anything but calm beneath the surface. US value, equal-weight, and small- and mid-cap indices have quietly outperformed. In contrast, US large growth has fallen meaningfully, and global software has suffered a deep drawdown. This is not a classic ‘rates up, growth down’ trade, and it does not feel like a normal cyclical rotation either. It is a repricing of both duration and competitive moats.

What has changed since November is the market’s willingness to pay a premium for perceived scarcity. For most of the last decade, investors were rewarded for owning businesses with the strongest network effects, the highest incremental margins, and the longest duration of growth. That model still exists, but a new reality is challenging it. AI is lowering the cost of building and distributing digital capabilities, while the big platforms are becoming more capital-intensive as they race to build the infrastructure. The result is a market that is simultaneously questioning the durability of some software moats and demanding proof that hyperscaler AI spend can translate into sustained earnings.

This is why the sell-off in software has been so forceful. The market has moved from treating AI as a tailwind for the sector to asking whether parts of the software stack are vulnerable to disruption. Recent moves have broadened beyond software into wealth managers, insurance brokerage, tax and accounting services, data providers and legal research. More recently, the ‘AI immunity’ positioning has even reached parts of the physical economy that investors would not normally consider digital, including office REITs, trucking and logistics. In truth, this is less about AI making whole industries obsolete overnight and more about markets wrestling with a genuine ‘known unknown’. If the pace of change is accelerating, then the visibility of future earnings becomes harder to underwrite, particularly for businesses priced at premium multiples.

However, there is an important nuance here. The idea that investors are ‘fleeing the digital world’ can be taken too far. Many of the companies being sold are likely to benefit from AI through higher productivity, better customer targeting, and lower cost-to-serve. The market is right to recognise that competitive dynamics will shift, but it is also capable of overshooting, particularly when positioning becomes crowded. The most plausible medium-term outcome is not that ‘software is dead’, but that the dispersion within software widens. Platforms, embedded workflow systems, security and infrastructure are likely to prove more resilient than narrower ‘single feature’ tools that can be replicated more easily.

The same scepticism is now being applied to the mega-cap growth complex. Investors are no longer rewarding capex plans simply because they are large. The question is increasingly about return on invested capital. This is why the market has at times appeared to punish good earnings. It is not rejecting AI. It is challenging the timing of payback.

US Macro data

Last week reinforced the ‘late-cycle but still alive’ feel. US payrolls rose by 130,000, and the unemployment rate unexpectedly fell to 4.3%. The headline number looked strong, but the annual revisions were a meaningful reminder that hiring has slowed considerably over the past year, with job gains revised down sharply. Even so, the composition of hiring was constructive. Health care continued to lead job growth, with construction, and professional and business services also adding jobs, and manufacturing posting its first monthly employment gain in more than a year. For markets, the immediate impact was in rates. Treasuries sold off as traders pushed back expectations for the next Fed cut, with the front end moving quickly as the labour market data reduced the urgency for easing.

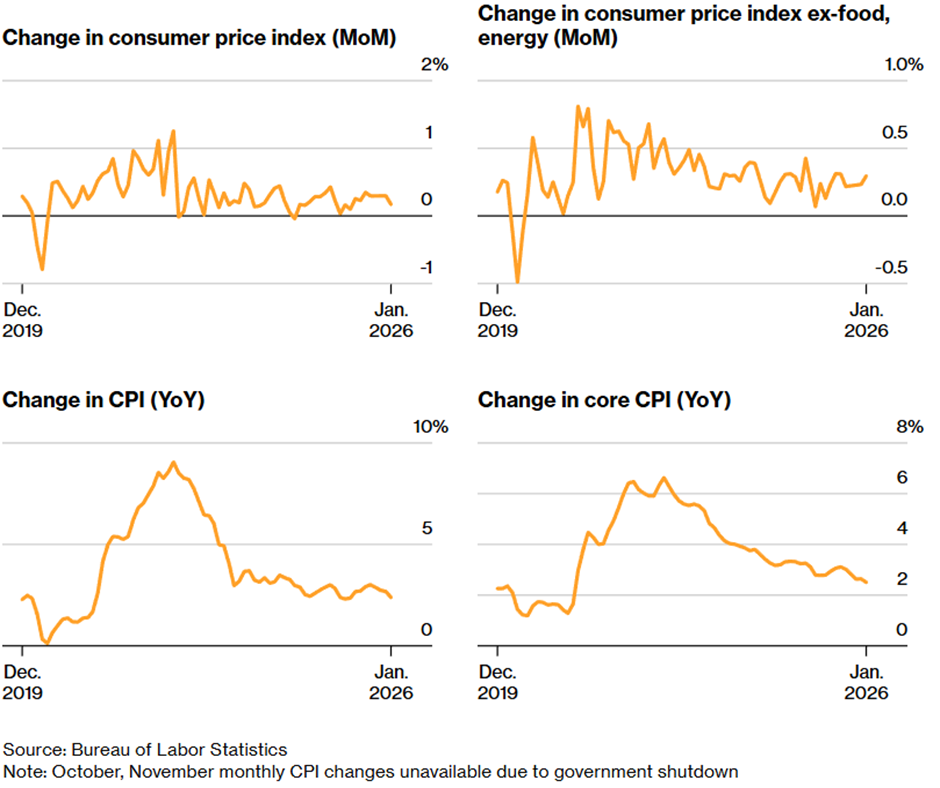

Later in the week, inflation data provided the counterbalance. January CPI was milder than feared. Headline CPI rose 0.2%, and core CPI was 0.3%, with the year-on-year core rate easing to 2.5%, the lowest since 2021.

Energy helped, and core goods remained stable, while shelter inflation also looked better behaved, with a smaller monthly rise than recent prints. Services inflation was firmer, but the overall tone remained encouraging, particularly against the backdrop of recent years, when January seasonality has often produced unpleasant upside surprises. Markets took the report as a modest relief, with yields easing and risk appetite improving into the close. Real wage data also moved in the right direction, with inflation-adjusted earnings improving, which is crucial for the sustainability of consumer spending.

Earnings season

Continues to provide a fundamental anchor for a market busy debating disruption and valuation. With roughly three-quarters of the S&P 500 having reported, results remain solid. The proportion of companies beating EPS expectations is slightly below the five-year average. Still, the magnitude of surprises is close to normal, and the blended earnings growth rate for Q4 is now running at just over 13% year-on-year, marking a fifth consecutive quarter of double-digit earnings growth. Revenue growth has also been robust, with the blended sales growth rate near 9%, the strongest since 2022, and the vast majority of sectors delivering year-on-year gains. To reiterate an earlier point, the market’s anxiety is not being driven by a threat to profits now; rather, it is how profits might be shared and defended as AI shifts competitive dynamics.

Japan

Was the standout last week. Markets responded positively to Takaiichi’s success and the clearer pro-growth message coming from Tokyo. Japan remains exposed to currency and rate volatility, but investors continue to lean into the structural story of governance reform, higher shareholder returns and rising corporate focus on profitability. The price action last week suggests that investors still want diversification away from the most crowded US growth trades, and Japan continues to benefit from that rotation.

UK

Gilts were better supported over the week. Political noise did not translate into a new bout of instability, with Starmer surviving a challenge linked to the Mandelson controversy, and markets treating that outcome as a small positive for domestic policy continuity. That helped reinforce the idea that the UK is not the source of global risk as it has been at times over the past two years, even if fiscal constraints remain a structural issue.

This week…

Has a few genuine diary items rather than just noise. In macro, the focus is on February flash PMI surveys, UK inflation data, and a heavy Japan calendar including inflation and Q4 GDP, while in the US, attention turns to the Fed’s reaction function via the FOMC minutes alongside the key ‘hard’ prints with Japan Q4 GDP and the PCE inflation release. Asia will also be operating in a holiday-disrupted rhythm as the Lunar New Year begins, with Chinese New Year’s Day falling on Tuesday.

This is the start of the Year of the Fire Horse, which is traditionally viewed as a high-energy, risk-taking year, and while markets do not trade astrology, the holiday period can still matter in practice. Liquidity is often thinner, trading volumes lighter, and price action can be more technical than fundamental.

With a slightly broader focus across the world-stage risk calendar, the US Supreme Court tariff ruling remains a live catalyst, while in earnings, the next major milestone for the AI complex is Nvidia, which reports next week and will be watched closely for any sign that demand, utilisation and pricing power remain as strong as the industry claims.

This content is intended for financial professionals only. These are the author’s views at the time of writing and may be subject to change. This content is not intended to provide the basis for any investment advice or recommendation. Any forecasts, figures, opinions, tools, strategies, data, or investment techniques are included for information purposes only.

The information presented is considered to be accurate at the time of production and has been obtained from or based upon sources believed by the author to be reliable and accurate, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Please visit our Regulatory Information and Terms of Use pages for more information.

Production

Production