The rule of law meets the rule of Trump!

Author: Tom McGrath, Head of MPS, 8AM Global

Market Overview

Markets closed the month with a touch more calm, but clarity remains elusive. Once again, tariffs, courts, and selective optimism vied to claim the market narrative. Early in the week, investors leaned into the so-called ‘TACO trade’ – Trump Always Chickens Out – after a federal court temporarily appeared to have reversed all of Trump’s reciprocal tariffs. But hopes of a reprieve evaporated just as quickly, with an appeals court stepping in to reinstate the tariffs and extend the uncertainty. Nevertheless, May 2025 has to go down in the history books as a successful one for equity investors, and those ‘who sold in May’ will be wishing they hadn’t observed that old investor idiom!

US Policy

The latest legal seesaw says more about the current climate than the tariff policy itself. Economic direction is now as likely to come from courtrooms as it is from the Fed or Treasury. With tariffs firmly back on the table and now tangled in a legal process that could take months to resolve, markets, households, investors, and central banks are left trying to read the runes. Financial markets love an acronym, and ‘TACO trade’ might be the most fitting of the cycle. It captures the familiar rhythm of Trump threatening tariffs, markets flinching, and then a walk-back that revives risk appetite.

I did flinch when I first read that acronym, and all I could think was, ‘Please don’t tell him’, as a journalist did last week. But now he knows, and, for a man with an enormous ego, I thought he dealt with it well, chalking it up to ‘negotiation’, setting the opening bid absurdly high, then reeling it back to something more digestible. It’s a dance investors are getting to know well. However, the longer it persists, the less it resembles a strategy and the more it resembles noise. And if one day the promised tariffs do materialise or the legal brakes are removed, markets could find themselves mispriced with real consequences, but until then, the dance goes on.

The issue isn’t just volatility. It’s an erosion of trust in those who govern. Erosion of policy clarity, of institutional guardrails and of the assumption that threats are always hollow. Markets can handle drama. What they’re less good at is drift, where policy direction is unclear, and accountability keeps shifting. With the Fed on hold, courts in play, and tariff uncertainty lingering, the next phase may be less about rebounds, and more about recalibration.

US economy: Still growing – but noisy under the hood

We received the update on Q1 GDP data last week, and beneath the surface, the US economy remains more resilient than it initially appears. Yes, headline GDP dipped, which is unusual outside of a recession; however, the weakness was primarily due to volatile components like trade flows and inventories. A big surge in imports (mainly front-loaded ahead of tariffs) dragged the number lower. Strip that out, and core domestic demand was firmer than expected.

Real final sales to private domestic purchasers are (in my opinion) the best proxy for underlying momentum and grew steadily. Equipment investment even surprised to the upside, buoyed by aircraft and IT spending. But those gains likely reflect short-term reactions to tariff threats, not long-term confidence. And with inventories having added heavily to Q1 growth, the risk is that they become a drag in Q2.

The balance of risks is still shifting, and, without a doubt, the possibility of a recession is higher now than it was at the start of the year; however, the economy continues to defy the doomsayers. The job market remains central to this. Youth unemployment is rising, partly due to AI-related disruptions, and broader hiring momentum is softening. But there’s no sharp deterioration yet. If layoffs stay low and incomes hold up, the economy looks like it can still skirt around a downturn.

The Fed: No cuts, no panic

For the Federal Reserve, the data presents a puzzle with familiar pieces. Inflation is cooling gradually but not decisively. Core PCE, the Fed’s preferred inflation gauge, is at 2.5%, still above target but heading in the right direction. The headline PCE deflator is even closer to the goal, rising just 2.1% year-on-year – its best reading since early 2021.

That alone would be enough to keep the Fed patient. However, the tariff story complicates the matter. Most goods currently being sold were imported before the new duties kicked in. As those inventories run down and replacement stock arrives at a higher cost, we’ll likely see inflation creep back up midyear. How much of that gets passed on to consumers, or absorbed by company margins remains to be seen.

The Fed won’t want to misread this moment. Policymakers recall the 1970s when unanchored expectations led to long-term damage. The risk now isn’t hyperinflation but the perception that the Fed might blink too soon. As such, expect no change at the upcoming FOMC meeting. The updated dot plot will matter more than the press conference. Doves will take comfort in softer inflation. Hawks will worry about what’s still to come. Most will remain firmly in wait-and-see mode until there’s more clarity on tariffs.

Consumers: Cautious but capable

The good news is that household income continues to rise. In April, wages and salaries posted a healthy 0.5% gain, pushing real disposable income up by 0.7%. Over the past three months, that figure has risen at an annualised rate of 7.5%, a pace not seen since the stimulus-fuelled rebound of early 2023.

But spending didn’t follow. Real consumption barely budged in April, after a stronger March that likely reflected consumers pulling forward purchases ahead of expected price hikes. The drop in consumption growth from 1.8% to 1.2% in the revised Q1 GDP numbers suggests households are entering a more cautious phase. The savings rate jumped to a one-year high of 4.9%, raising the question: are consumers battening down the hatches or simply waiting to spend government transfer income later? It’s likely a bit of both. Sentiment remains fragile, and tariff headlines continue to play a bigger role in shaping household psychology than the economic fundamentals alone might suggest.

UK outlook: Quiet resilience turning louder

While the US wrestles with legal wrangling and policy noise, the UK has quietly delivered a string of better-than-expected data. Business confidence bounced back sharply in May, with the Lloyds Business Barometer hitting a nine-month high. The rebound erased April’s tariff-driven dip and brought sentiment back to levels last seen after Prime Minister Keir Starmer took office. By way of comparison, the UK Savings rate is comfortably back above 10% of income, which suggests consumers are in a better place.

Much of the gain in confidence reflects a broader sense of economic stability. The UK economy grew at its fastest pace in over a year in Q1, retail sales are running strong, and inflation expectations have moderated. The improvement comes despite lingering concerns over tax hikes and budget cuts, which had previously rattled households and corporations alike. The mood is increasingly one of cautious optimism rather than crisis management.

Notably, the Lloyds survey suggests that companies are planning to expand headcount again while wage expectations remain robust. Business inflation expectations also fell back in May, reversing the uptick seen in April. Services firms are leading the charge, but construction sentiment is also improving, and regional confidence is broadening. Adding to the positive tone is the state of the UK consumer. Retail sales in April rose a striking 1.3% month-on-month, far ahead of the 0.1% increase forecast by economists. Despite concerns that Trump’s tariff threats would spook households, the data show that spending surged, likely helped by the good weather. Nevertheless, it’s the fourth consecutive month that retail sales have beaten expectations. Over the three months to April, sales were up 2.8% year-on-year, the strongest performance since 2022.

These numbers support the view that the UK economy is not only holding up but may be gaining pace. Even with rising bills and lingering trade uncertainties, consumers continue to open their wallets. If sentiment and income trends remain stable, this momentum can carry through the rest of the year. While not immune to global volatility, the UK may be in a better position than many expected, thanks to a calmer political climate, a focus on fiscal credibility, and tentative signs of real wage growth. The challenge now is to turn resilience into a sustainable recovery. It is always a good sign to me when I see UK Small and Mid-Cap outperforming large cap…

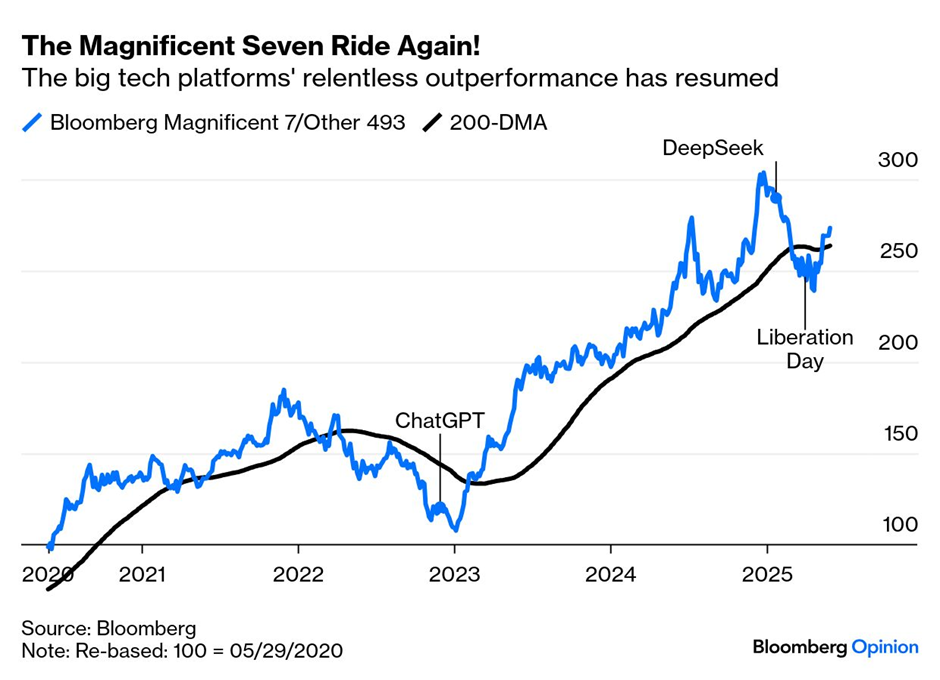

Nvidia: AI’s bellwether still rings true

Arguably, the biggest news last week, if you were to ignore the huff and puff from The White House, was the release of Nvidia’s Q1 earnings, and to paraphrase Mark Twain, it would now seem that rumours of Big Tech’s demise have been greatly exaggerated. If ever there were a bellwether for the AI boom, Nvidia is it, and it just posted another blockbuster quarter.

Sales have surged since the launch of ChatGPT, thrusting AI hardware into the spotlight, and Nvidia has ridden the wave with a rare mix of scale and profitability. Yes, margins slipped slightly due to inventory write-offs linked to blocked shipments from China, but they remain in jaw-dropping territory. More importantly, the top-line growth continues to exceed expectations. The bigger takeaway is that the broader AI trade isn’t over. The so-called ‘Magnificent Seven’ mega-cap platform stocks, led by Nvidia, have resumed their outperformance. What initially appeared to be a major reversal earlier this year is increasingly resembling a healthy correction.

This pace of growth won’t last forever. There are valid questions about whether demand for AI chips can remain this elevated or whether competition will eventually pressure margins. But the idea that the bubble burst long ago is nonsense to me. I happen to think we are closer to the beginning of the AI revolution than to its end, and that the AI trade remains very much in play.

Looking ahead: What’s on the radar this week?

This week brings a mix of macro and micro events that could shape sentiment heading into June. In the US, the focus will be on Friday’s non-farm payrolls report, which will offer the clearest read yet on whether the labour market is cooling. Wage growth and participation rates will be under scrutiny, especially as the Fed weighs the balance between sticky inflation and slowing momentum. Before that, we’ll get the ISM services index and factory orders, which should give a pulse check on the health of both the consumer and the broader economy.

In Europe, the ECB is widely expected to cut rates, marking a notable divergence from the Fed. Markets will be looking beyond the cut to see how forcefully policymakers guide the path ahead—whether this is a one-off move or the start of a broader easing cycle. Meanwhile, Chinese trade data is due mid-week, offering a window into global demand and whether the tentative recovery in Asia is building pace.

On the micro side, it’s a quieter stretch for earnings, though a few US retailers and industrials are set to report. Their updates could provide useful signals on consumer resilience, input costs, and inventory management. Any commentary on tariffs or shifting supply chain dynamics will be closely parsed. And, as ever, markets will be watching Washington, both for signs of a thaw in trade negotiations and for how the legal battles around tariff authority continue to unfold in the background.

This content is intended for financial professionals only. These are the author’s views at the time of writing and may be subject to change. This content is not intended to provide the basis for any investment advice or recommendation. Any forecasts, figures, opinions, tools, strategies, data, or investment techniques are included for information purposes only.

The information presented is considered to be accurate at the time of production and has been obtained from or based upon sources believed by the author to be reliable and accurate, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Please visit our Regulatory Information and Terms of Use pages for more information.

Production

Production