Trump 2.0 & an all time high for the FTSE 100!

Author: Tom McGrath CIO, 8AM Global

’Twas the week before Trump, and all through the Street,

Markets were nervous, bonds faced retreat.

Inflation was rising, both Stateside and Brit,

With fears of more tariffs adding to the hit.The pound took a dive, retail sales sank low,

While Tesla kept climbing, stealing the show.

Crypto was buzzing, as volatile as ever,

Its bulls proclaiming, “It’s now or never!”But bonds found their footing, yields tighter to close,

As the markets prepared for what Trump might impose.

The world watched and waited, with cautious delight,

For the dawn of a new era, fast taking flight.Penned by Chat GPT 4 with only minor prompting by Tom McGrath – Jan 2025

Market Overview

What a difference a week can make in market sentiment. This time last week, I was proclaiming the end of Goldilocks, setting the scene for a bit of a market correction and speculating that the US 10-year yield could hit 5% soon. Roll forward just seven days, and thanks to some softish inflation data, it would seem that Goldilocks wasn’t quite ready to ‘exit stage left’, and investors have decided the glass is half full again. The upshot for markets was a slingshot rebound in both equities and bonds, not just in the US but also in Europe and the UK, where our very own multi-national FTSE 100 index turned in a new all-time high above 8500, about 50 points higher than the previous record set in May last year.

So what changed? Part of the reason must be attributed to better-than-expected economic data, specifically inflation and part of the Big Bank earnings. However, a chunk of the feel-good factor must go down to Trump coming into the presidential office on Monday as investors wanted to get ahead of another potential Trump Bump and historical precedence that markets do well in the 3 months post-inauguration. We shall find out later today if we get any fireworks – both Tesla and Bitcoin enjoyed a good week – and they are the most likely to benefit from any euphoric investor action.

It was one of those ‘phew’ moments when we got Wednesday’s US inflation data showing that price increases are continuing to moderate. While this triggered a substantial ‘risk-on’ rally, it also underscored the heightened anxiety that had gripped markets. The numbers were only slightly better than expected, signalling progress in controlling inflation, but they offered little in terms of a clear roadmap for what lies ahead. While investors chose to put a positive Goldilocks spin on the data, I wouldn’t leap to the same conclusion, and the jury is still out on additional rate cuts from here.

US

A closer look at the US Consumer Price Index (CPI) reveals that food prices remain on an upward trajectory, although the pace has significantly slowed compared to the surges of 2022. Whilst energy and goods prices remain relatively stable, a simple glance at the Oil price over the last month (+10%) suggests that it could become a new headache very soon. Tuesday’s PPI data was also lower than expected but still ticked upward. The upshot of the softer-than-expected inflation numbers was an increase in the expectation for rate cuts this year. Markets have now nailed on one 25-basis-point rate cut this year, with the likelihood of a second cut climbing to 57%, up from 24% prior to the release of CPI data. Interestingly, these probabilities have only returned to levels seen before last Friday’s strong US unemployment figures. So, despite the buzz surrounding the latest data, the market’s actual view on the Fed’s near-term trajectory remains largely unchanged and makes me think both bonds and equities might have got a bit carried away.

I was more interested in seeing the big recovery in US manufacturing, housing surging, and the upward revision in GDP growth from the Atlanta GDPNow Index (+3% Q4 2024). Now, that is the type of old-fashioned ‘good news’ that used to drive equity markets higher back in the old days before we had all this ‘bad news is good news’ and ‘good news is bad news’ nonsense. I am getting nostalgic, but a stronger economy is ultimately going to drive those earnings higher, even if we don’t end up with as many rate cuts as people would want.

Speaking of earnings, they kickstarted this week when we got reports from the Big Banks, and for the first time in a long time, we got everyone coming in ahead of expectations. That was enough to drive overall analyst earnings estimates for Q4, an entire percentage point higher to growth of 12.5% year-on-year. From here, results pour in thick and fast as we get Netflix, Johnson & Johnson, Proctor & Gamble and American Express, amongst others, next week, so we will soon get a feel for how things are going.

UK

The FTSE 100 finally set another all-time high, surpassing and closing above 8500 for the first time. There were many contributing factors at the macro and company levels. Still, I suspect the primary reason was relief that the UK’s borrowing costs have seen their largest three-day drop in over a year, with 10-year yields falling 25 basis points. This drop has spurred expectations of Bank of England rate cuts to support growth, strengthening bonds but pressuring the pound, which remains vulnerable. Chancellor Rachel Reeves will have no doubt slept (a bit) better at the news but not soundly, as the drop was probably due to data pointing to a weakening UK economy rather than any renewed faith in her government’s managerial abilities.

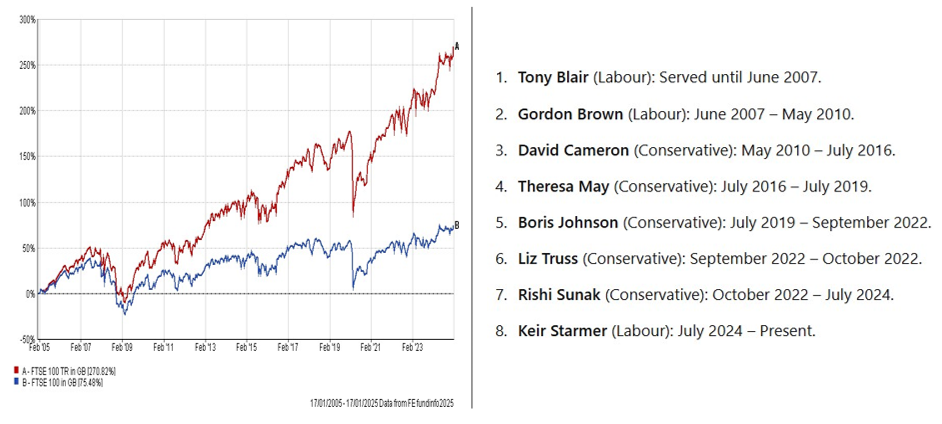

To celebrate, I have produced a graph that shows the FTSE 100 in all its glory. Now, I know the US has been the only market that anyone has been interested in over the last 20 years, but the FTSE 100 hasn’t done all that bad, all things considered (war, pandemic, financial crisis, Liz Truss, Boris …there are probably more I’ve not thought of…).

One thing that is often overlooked when we see news of the FTSE on a daily basis is that it is only the headline ‘Price Index’ that is quoted, and it ignores the ‘Total Return’ component that includes dividends, which are currently running a little under 4%. That explains the massive difference between the total return the index has achieved over the period, +270% versus 75% for the price level. For the S&P 500, Nasdaq, Eurostoxx, Nikkei and most global indices, the difference is nowhere near as acute because they don’t pay the same level of dividends (S&P 500 around 1.35%), so the FTSE doesn’t always get a fair comparison.

Back to the cause of the bounce, and I am afraid to report this is another of those ‘bad news is good news’ updates, which are probably just bad news over the long term! Retail Sales fell more than expected, and UK GDP Growth was an anaemic 0.1% for November, less than the 0.2% expected.

In case any of you eagle-eyed economic buffs counter this slight to our growth by pointing to the fact that the IMF upgraded the UK’s outlook for 2025 from 0.1% to 1.6%. This modest revision still contrasts with the UK’s OBR projection of a 0.5 percentage point boost from the October budget and suggests one big black hole in the UK’s budget. That is why we are seeing Sterling come under pressure and why I do not think the Gilt market is out of the woods yet by any stretch.

The coming months will be pivotal for Chancellor Reeves as she awaits the Office for Budget Responsibility’s (OBR) verdict on the UK economy’s potential growth rate. The watchdog’s reassessment, expected in its new forecasts on March 26 or delayed until autumn, could weigh heavily on the government’s fiscal plans and potentially trigger another Gilt scare.

So what should we expect from the BOE, given the fact economic growth is now confirmed as slowing? Surely, it must cut rates to get things going, and what better time than now, following a lower-than-expected reading in our inflation data when we got the news last week that CPI unexpectedly slowed to 2.5% in December. I think we may get a rate cut in February’s BOE update. If they don’t, they might not get the same window of opportunity for a while, as the next couple of CPI prints will likely be higher.

Reeves and the BOE got a lucky break in the CPI numbers as a closer examination suggests that this decrease may be more of a statistical quirk than a genuine economic improvement. The Office for National Statistics collects pricing data during specific periods each month. In December 2024, data collection coincided with Christmas Eve and New Year’s Eve dates when businesses offered promotional rates. This timing led to artificially lower recorded prices for services such as airfares and hotels, which accounted for all the drop, if not more, and that’s going to reverse with a fright next month!

Contrarian Corner: China

Did you know that in 2017, during Trump’s first year in office, the Chinese equity market went up more than 50% despite all the blustering about tariffs?

Donald Trump and Chinese President Xi Jinping spoke last week, discussing trade, fentanyl, and TikTok, just as a U.S. court ordered ByteDance to divest its U.S. operations. Both leaders called the talk positive, with Xi congratulating Trump and emphasising the need for stronger communication. Their conversation also touched on global issues like Ukraine and the Middle East, hinting at a potential thaw in U.S.-China relations despite prior tensions.

China’s market valuations remain historically low despite the September rally following Xi’s s ‘whatever it takes’ sentiments to revive their market. However, years of underperformance, weak corporate profitability, regulatory hurdles, and sluggish domestic consumption have left the market depressed. Critics argue these challenges justify the low valuations. However, there is a wind of change as the Chinese government is taking action, introducing stimulus to stabilise property and equity markets while shifting the economy toward domestic consumption. While results will take time, leadership’s commitment to structural reform and growth is clear, and the authorities stand ready to unleash the next round of measures once they have clarity on what Trump is planning.

China is investable, but probably selectively. For the moment, you might be better off sticking to the big tech stocks, as they offer strong earnings growth at valuations far below global peers. With improving macro conditions and undervalued high-quality businesses, investors shouldn’t ignore China.

So, by the time you read this, Trump will be about to be sworn in, and the world will look a lot different. He is better prepared this time and has assembled a cast of bright, motivated ‘yes’ men and women, and he controls both the House and the Senate, so the scene is set for a high-octane action movie with him playing the lead. I am nervous about what might go wrong but also excited about what could go right. Buckle up, and let’s try to enjoy the ride!

This content is intended for financial professionals only. These are the author’s views at the time of writing and may be subject to change. This content is not intended to provide the basis for any investment advice or recommendation. Any forecasts, figures, opinions, tools, strategies, data, or investment techniques are included for information purposes only.

The information presented is considered to be accurate at the time of production and has been obtained from or based upon sources believed by the author to be reliable and accurate, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Please visit our Regulatory Information and Terms of Use pages for more information.

Production

Production