S&P 500 sets a new record as Middle East Calms

Author: Tom McGrath, CIO, 8AM Global

Market Overview

As we near the end of the second quarter, US Equities surged to new all-time highs, defying the usual post-conflict caution and brushing aside another week of tariff noise. The S&P 500 powered past its February peak to close above 6170, capping a rally that has now added over 10 trillion dollars in market value since the April low. Nvidia flirted with the $4 trillion mark! The dollar weakened, slipping to its lowest level in nearly three years. Treasury yields fell, with the 10-year Treasury dropping toward early May lows. Oil prices retreated sharply, while investor sentiment remained buoyant. A rarity in 2025, large-cap UK and European markets haven’t kept pace with the US this month, but currency-adjusted returns were much more level-pegging, and UK mid and Small-caps continue to recover strongly.

What made the US equity rally even more impressive last week was that it unfolded in the shadow of a war scare. Days after US airstrikes hit Iran’s nuclear facilities, President Trump abruptly declared the conflict over, brokering a ceasefire that both Israel and Iran, somewhat remarkably, accepted. That lifted a major tail risk off the table, helping oil collapse back to pre-conflict levels and allowing markets to breathe a collective sigh of relief. Outside of the ME conflict, the market had plenty more to digest. Trump’s whiplash diplomacy on trade, a fresh batch of sticky inflation data, and a drop in consumer spending that was the steepest since January. However, I think it was telling that traders chose to focus on positives: a resilient US economy, a Fed still likely to cut rates, and hopes for softer inflation once the current tariff spikes pass. I am not sure I completely ‘buy into’ this rally, but I think it would be foolish to stand in the way of a charging bull at the moment.

US economics

Still, under the surface, the economic picture remains mixed. The latest personal spending figures painted a more fragile backdrop. Real consumer outlays fell 0.3% in May, marking the sharpest decline since the start of the year and a broad-based drop across both goods and services. That included weaker demand for transport, dining, travel and financial services, all categories sensitive to sentiment. The data confirms that household demand has softened meaningfully since the start of the year, weighed down by tariff uncertainty, falling transfers, and a gradual erosion in confidence. While wages rose again, helping offset some of the drag, personal income fell for the month, and the saving rate dipped to just 4.5%. Core PCE inflation nudged slightly higher but remains well contained. In short, the consumer still has spending power but is showing signs of restraint just as policymakers start to assess how deeply tariffs may cut into demand in the coming quarter.

The shifting backdrop is presenting the Federal Reserve with a dilemma. Powell has warned that tariffs are likely to lift inflation in the coming months, but if those pressures fail to materialise, the door remains open for rate cuts. Markets are still pricing in at least two cuts before year-end, with growing conviction that September could be the turning point. Several Fed officials have hinted as much, with Kashkari even floating the possibility of two cuts this year if growth stalls.

But the Fed is not just battling data uncertainty. Political pressure is also building. Trump has made little secret of his frustration with Powell’s reluctance to act quickly and has dropped hints about naming a potential successor more aligned with his own pro-growth instincts. While no formal move is expected before the election, the suggestion alone adds to the sense that Powell’s independence is being tested just as policy becomes more finely balanced. With inflation expectations stable and consumer demand softening, investors are betting that the Fed will ultimately err on the side of caution. However, the politics of monetary policy are intensifying, and Powell may have less room to manoeuvre than usual.

Tariffs

That muted consumption backdrop adds further weight to the argument that tariff risks are more than just noise. Markets may still be hoping that Trump’s July 9th deadline passes without incident, but signs of escalation continue to build. The president has hardened his stance in recent days, threatening to impose 25% levies on countries that fail to strike deals while hinting that even the currently prescribed window for negotiation could be shortened. Treasury Secretary Scott Bessent tried to inject some calm, suggesting partial extensions might be granted through to Labour Day. Still, the overall message was unmistakable: patience is wearing thin, and not every partner will be spared.

Trump’s decision on Friday to terminate trade talks with Canada over its digital services tax underscored just how quickly the mood can turn. While the tax had long been in the pipeline, its retroactive nature and targeting of US tech giants proved too much for the White House to stomach. The Canadian dollar slumped, and trade-sensitive stocks fell as markets digested the shift. And it wasn’t just Canada in the crosshairs. Despite securing headline deals with the UK and China, Trump warned that many countries were still lagging behind and could soon face higher tariffs. Negotiators are scrambling to finalise a slate of top-ten trade agreements, but the clock is ticking, and markets, for now, appear complacent about what happens if they fall short.

Europe & NATO

While the US contends with slowing consumer demand and rising tariff tensions, Europe has quietly undergone a strategic shift of its own. Last week’s NATO summit in The Hague marked a milestone in transatlantic relations and a significant moment for European defence, with far-reaching implications for fiscal policy, industrial strategy, and financial markets.

Markets may have been distracted by tariff headlines, but the real story was the alliance’s agreement to ramp up military spending beyond the longstanding 2% GDP threshold. The new target of 5%, including 3.5% for core defence and 1.5% for broader security infrastructure, was framed as a necessary response to Russia’s ongoing threat. However, it was also a major political victory for Donald Trump, who used the summit to pressure allies into faster rearmament and to renew the US commitment to collective defence despite prior scepticism.

Germany, long a laggard in defence outlays, has now pledged to build Europe’s most powerful conventional military. At the same time, even hesitant partners like France and Italy have quietly signed up to more ambitious procurement schedules. That rearmament drive could unlock trillions in defence-related investment over the next decade, supporting industrial production, boosting aerospace and technology suppliers, and accelerating the reshoring of critical capabilities, such as cybersecurity and munitions manufacturing.

Yet the economic trade-offs are real. With debt levels already high and growth fragile across the eurozone, the path to 5% will strain fiscal balances unless offset by cuts elsewhere or looser EU rules. Spain and Slovakia have already voiced concern, while markets will be watching how this shift interacts with broader European recovery efforts. The move may help anchor NATO unity, but it will also add another layer to Europe’s already complex fiscal landscape, one that bond investors and credit agencies will not ignore.

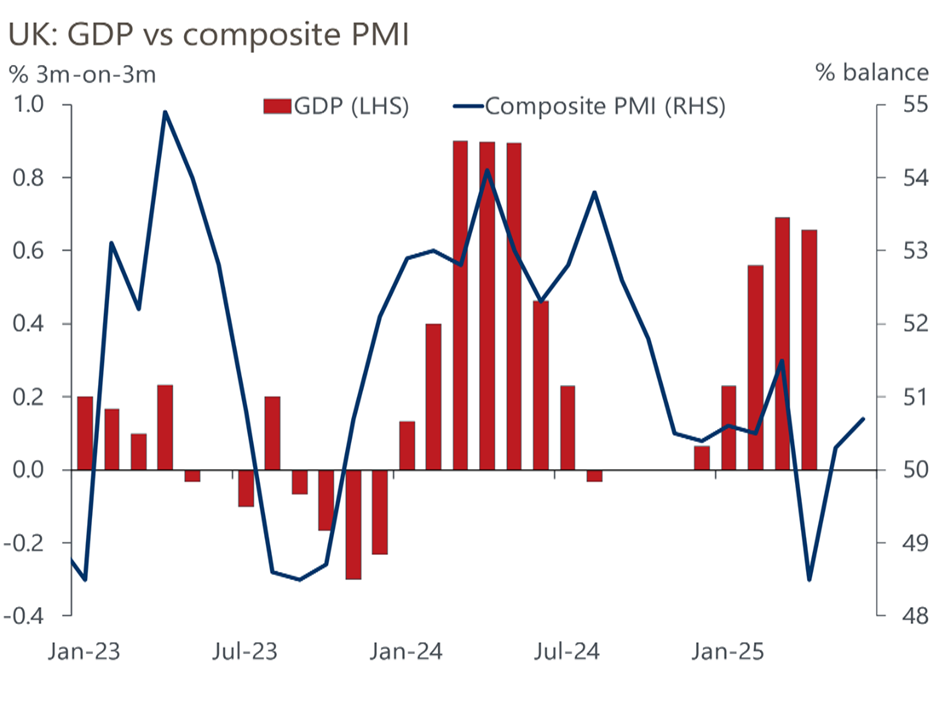

UK rate cuts coming?

In a quiet week for data releases, the spotlight turned to the Bank of England, with three MPC members offering fresh insight into the balance of views behind last week’s dovish hold. Deputy Governor Dave Ramsden used his speech at the Barclays-CEPR Forum to justify his vote to cut, citing clear signs of slack in the labour market and flagging HMRC data showing lower-paid private sector employment contracting. He warned that the hiring slowdown could deepen in the months ahead, increasing the risk that inflation settles below target without a looser stance.

Governor Andrew Bailey struck a similar tone, noting that monetary policy remains restrictive and that a ‘gradual and careful’ path to easing is still appropriate. While he didn’t give a clear steer, the language remains consistent with a quarterly cutting cycle, making an August rate move likely if labour and inflation data don’t surprise the upside. Megan Greene was more equivocal. While she warned that elevated inflation expectations could drive persistence in price setting, she also endorsed a cautious approach to easing. With a dovish majority already forming, Greene’s vote may not prove pivotal.

The June flash PMI offered little encouragement. The composite index ticked up to 50.7 from 50.3, leaving the Q2 average just below the ‘no change’ threshold consistent with flat GDP. Firms continued to cut jobs, and both input costs and selling prices eased again, reinforcing the case for further policy loosening.

One Big Beautiful Bill Act (OBBBA)

And finally, the weekend brought a political breakthrough that could yet carry market implications. President Trump’s flagship $4.5 trillion tax cut and spending bill (officially called OBBBA) cleared a major Senate hurdle late Saturday after hours of tense backroom negotiation. The 51–49 vote to begin formal debate suggests that Republican leadership is edging closer to securing the votes needed for final passage ahead of Trump’s self-imposed 4th July deadline.

The bill’s sheer scale, combined with its inflationary potential, had been a source of friction within the GOP, with fiscal conservatives demanding deeper spending cuts and moderates pushing back on healthcare and green energy rollbacks. The latest version attempts to thread the needle, accelerating the wind-down of EV (Musk not happy!) and solar tax credits while creating new funds to cushion the blow to rural hospitals and Medicaid-dependent states. SALT deduction caps were temporarily lifted to appease coastal lawmakers, and further adjustments are expected before a final vote is taken.

Markets had begun to price in the risk of fiscal stalemate. But the sudden progress, if sustained, could reinforce expectations of stronger near-term growth and reignite debates around inflation and long-term debt sustainability. That might not faze equities in the short run, but bond markets will be watching closely. If OBBBA passes, the coming week could mark a pivot point not just for Trump’s economic agenda but for the entire macro narrative heading into the second half of the year.

What next?

For me, corporate earnings are crucial to long-term performance in the equity market. The forecast for only a 2.8% profit growth in Q2, the weakest in two years, leaves little room for error. Flows into U.S. equities have been relentless, exceeding $160 billion year-to-date, but this only increases the risk if earnings do not meet expectations. Currently, the market is banking on a soft landing: tariffs that remain threats without actual enforcement, a Federal Reserve that makes the right moves at the right time, and consumers who continue to spend. While this outlook isn’t irrational, it is starting to feel fully priced. OBBA’s progress contributes to the system but also creates significant pressure within it.

This week…

Key events to watch this week include the ISM manufacturing index on Monday, the JOLTS job openings report on Tuesday, the FOMC minutes on Wednesday, and the June non-farm payrolls report on Friday. Eurozone flash CPI is due Tuesday, and China’s Caixin manufacturing PMI lands the same day.

On the corporate front, earnings season edges closer with updates from Levi Strauss, Constellation Brands, and several early Q2 pre-announcements. US banks also appear at industry conferences, offering insights into lending, consumer trends, and credit quality.

This content is intended for financial professionals only. These are the author’s views at the time of writing and may be subject to change. This content is not intended to provide the basis for any investment advice or recommendation. Any forecasts, figures, opinions, tools, strategies, data, or investment techniques are included for information purposes only.

The information presented is considered to be accurate at the time of production and has been obtained from or based upon sources believed by the author to be reliable and accurate, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Please visit our Regulatory Information and Terms of Use pages for more information.

Production

Production