It’s getting uglier as Houthis join war: US troops arrive in Persian Gulf

Author: Tom McGrath, CIO, 8AM Global Ltd

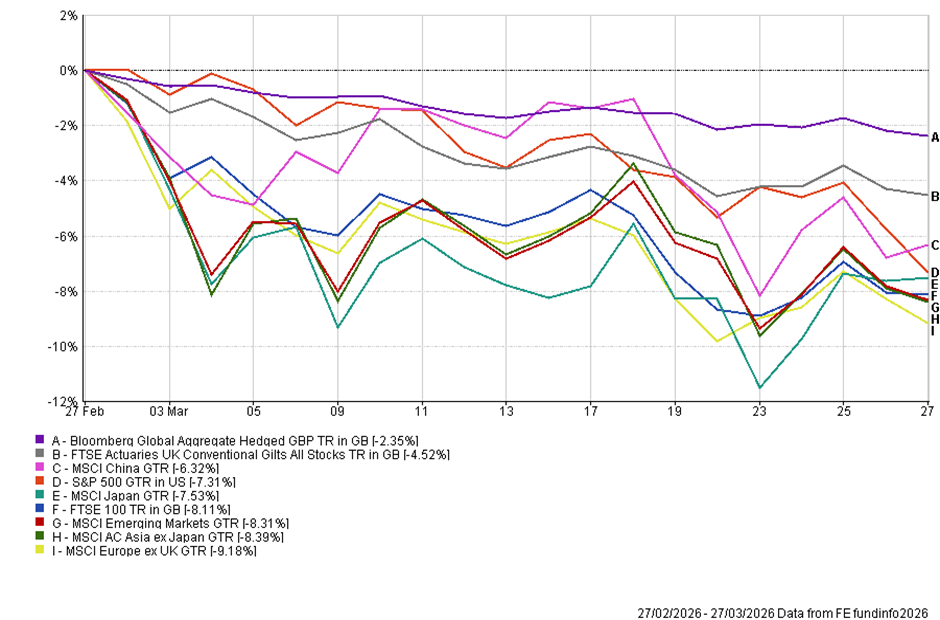

It was another bad week for markets, and this time the message was harder to ignore. Losses were broad, persistent and uncomfortable. Global equities fell sharply again, with the US joining other regional markets in correction territory. More notably, bonds failed to provide protection, with gilt and Treasury yields rising as equities fell. The chart below captures it well: this has not been a rotation; it has been a drawdown across almost everything. Markets had been relatively resilient through the early stages of the conflict, but over the last 10 days, the sell-off has accelerated, with investors now pricing in the consequences, not just the headlines.

What has changed is not simply that the Iran conflict continues, but that it is broadening and becoming more complex. Over the weekend, the war entered its fifth week, with the Houthis now more directly involved, continued strikes across the region and further US troop deployment signalling preparation for a more prolonged phase. The Strait of Hormuz remains heavily disrupted, and while Saudi Arabia has increased flows through its East-West pipeline, that workaround is partial and itself vulnerable if disruption spreads into the Red Sea. In short, this is no longer a contained shock. It is becoming a regional conflict with multiple pressure points, and markets are starting to reflect that.

The most useful way to frame this now is through scenarios. Our base case remains a prolonged standoff with controlled disruption, but the balance has shifted. We would now assign roughly 40% to a prolonged standoff, 20% to a negotiated off-ramp, 30% to broader military escalation or forced reopening of Hormuz, and 10% to a more severe energy infrastructure shock. The key point is not the precision of those numbers, but the direction: the probability of a clean resolution has fallen, while the risk of escalation has risen. Markets are adjusting to that reality.

That matters because the real issue is no longer the conflict itself, but what it does to the macro environment. Oil above $110 is not catastrophic in isolation, but it is high enough to keep inflation uncomfortably elevated and delay the policy easing markets had been expecting. At the same time, it is acting as a tax on consumers and businesses, eroding real incomes and confidence. This combination — sticky inflation and weakening growth — is exactly what makes this environment so difficult. It explains why equities have struggled, why bonds have sold off, and why traditional diversification has not worked as expected.

US

This is increasingly a late-cycle stress test. The hard data coming next week, jobs and retail sales will likely still reflect pre-conflict conditions and may look reasonably resilient. But the forward-looking indicators are starting to turn. Higher gasoline prices are already weighing on sentiment, equity market declines are beginning to hit wealth effects, and hiring remains subdued. Importantly, oil shocks feed through to the labour market with a lag, meaning the real economic impact is still ahead rather than behind us. The key nuance is that long-run inflation expectations remain anchored, which should give the Fed some flexibility, but the balance of risks is clearly shifting.

UK

The UK provides a more immediate and visible example of how this is feeding through. Mortgage rates have risen sharply, with the average two-year fix moving materially higher in just a few weeks, while fuel costs are increasing and consumer confidence has fallen back again. Households are cutting back on discretionary spending, particularly big-ticket items, and increasing precautionary savings. Crucially, this weakness was already emerging before the conflict intensified, meaning the energy shock is compounding an already fragile backdrop. That is why BoE rhetoric has been more cautious than market pricing suggests. Policymakers are increasingly focused on weaker demand and labour market slack, rather than assuming a repeat of the wage-price spiral seen in 2022.

Europe

Remains the most exposed major region. Higher energy costs are quickly feeding into inflation, while growth expectations are being revised lower. Industrial sectors, particularly energy-intensive ones, are already under pressure, and there is a growing risk that this pressure will spread more broadly as input costs rise and real incomes fall. The policy response is also more constrained, with limited fiscal room in many countries and an ECB that faces a difficult trade-off between inflation and growth. In effect, Europe is once again at risk of being the clearest expression of a stagflationary shock.

China

By contrast, China is more insulated at the consumer level but not immune. Its domestic energy mix and policy controls limit direct CPI impact. Still, higher input costs are likely to compress industrial margins, while softer global demand and tighter financial conditions weigh on exports. The pattern remains consistent with our broader view: resilience on the supply side, but still-soft domestic demand and limited ability to offset a global slowdown.

Fixed Income

One of the more uncomfortable features of the past few weeks has been the failure of traditional diversification. Bonds have sold off alongside equities as markets reprice inflation and rate expectations, while gold has been inconsistent, initially falling as real yields rose before stabilising more recently. This does not mean safe havens no longer work. It reflects the awkward phase we are in, a supply-driven shock that is pushing inflation higher while simultaneously weakening growth. If the situation escalates further, defensive assets are likely to reassert themselves, but for now, markets remain caught between competing forces.

Don’t panic out now!

There is a more constructive way to look at where we are. Markets have now moved a long way in a short period of time and are beginning to price a more realistic range of outcomes. Earlier in the conflict, resilience bordered on complacency. That is no longer the case. While risks clearly remain, particularly around further escalation or disruption to alternative energy routes, we are closer to the bottom of this adjustment than the top, provided the conflict does not deteriorate materially from here.

This week…

The focus will remain on both geopolitics and the data. On the geopolitical side, markets will look for any genuine signs of de-escalation, but rhetoric alone is unlikely to be enough. Developments around Hormuz, the security of the Red Sea route, and the behaviour of oil prices will be critical. On the economic side, US labour market and consumer data will be closely watched but should be interpreted with caution given the lagged nature of the shock. In the UK and Europe, further evidence of weakening demand and rising cost pressures will reinforce the current narrative. More broadly, the key question is whether the recent market moves are the beginning of a deeper downturn, or a painful but necessary repricing in response to a more uncertain world.

This content is intended for financial professionals only. These are the author’s views at the time of writing and may be subject to change. This content is not intended to provide the basis for any investment advice or recommendation. Any forecasts, figures, opinions, tools, strategies, data, or investment techniques are included for information purposes only.

The information presented is considered to be accurate at the time of production and has been obtained from or based upon sources believed by the author to be reliable and accurate, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Please visit our Regulatory Information and Terms of Use pages for more information.

Production

Production