China has ‘Whatever it takes’ moment!

Author: Tom McGrath CIO, 8AM Global

Market Overview

China dominated the headlines of the financial press last week, unleashing a stimulus blitz that resulted in the best week for their equities since 2008. That move dragged the Asian and Emerging Market Indices significantly higher and even Japan joined in on the act. That move overshadowed events in the West, but it is worth noting that several European Indices and both the Dow Jones and the S&P 500 chalked up new highs. Bond markets struggled to digest some strong economic news out of the US, but were comforted on Friday when inflation data came in favourably. Oil retreated again and Gold once more achieved new highs. Not much action in the currency markets as FX traders are struggling to coalesce on a new narrative for USD direction.

‘Whatever it takes’

I think it was only two weeks ago that I wrote I had just about given up on finding anything positive to write about China and that that, was probably positive, as it would surely mean a rebound was due. Little did I imagine the ensuing fireworks that would happen. Make no mistake, this was the Chinese authorities unveiling a financial bazooka targeted at kickstarting the economy and shoring up their property and financial markets.

So, what happened? Well, it started on Tuesday, where at a very unusual press conference held by the PBOC, which announced a range of monetary policy developments including a $114bn lending pool for institutions to buy shares. This had a positive effect on the market, but there was still a feeling of ‘nothing new here’ or ‘too little, too late’ and investors seemed unconvinced that the short term rally would hold.

But then on Thursday, at an unscheduled meeting of the Politburo with Xi Jinping present, we got an unequivocal sign that they meant business. Not only were more measures announced, but we got a clear commitment from the fiscal authorities that they were prepared to do ‘whatever it takes’ to boost the economy and support the property and equity markets. The key measures announced were designed to protect livelihoods by ensuring job opportunities for vulnerable groups, such as fresh graduates, migrant workers, the elderly and the disabled. There was also a focus on supporting low-income individuals and families with no employment. Additionally, the government announced plans to stabilise essential supplies, including food, water, electricity, gas, and heating, to safeguard living standards and prevent price volatility. It was an announcement short on detail but clear in intent, sufficient so far to instil a sense of confidence in investors that this might turn into a sustainable rally.

And then on Friday we got more concrete action and numbers to back up the rhetoric, as China’s central bank reduced the reserve requirement ratio by 0.5 percentage points, lowered the reverse repo rate from 1.7% to 1.5% and reduced borrowing rates for standing lending facilities by 20 basis points.

Turning around the property market, kickstarting the economy, and getting their population to start spending again, is clearly going to take some time, but financial markets on the other hand can react instantly, and react they did! The speed and size of the move has clearly left investors scratching their heads trying to work out what to do from here. Going in to this surprise turn of events, investors who manage global mandates had never in aggregate been more underweight China and they will be nursing big relative losses to index benchmarks. They now face a dilemma, do they now join in and close their underweights or wait for a pullback that might never happen.

The technical ratios are now showing very strong upward momentum with indices having surged above 200 day moving averages, suggesting that many might start recommitting funds to the region and that in turn could add further impetus.

Having historically been very covert in thoughts and actions, China has just executed good messaging and delivery, that will go some way to restore the confidence of foreign investors. Bulls are already suggesting that this could be the start of a long term re rating of Chinese assets, which have a long way to go before seeing comparable valuations to Western Assets. There are also positive ramifications for the rest of the world. With China providing implicit support for their equity and property markets and the Dragon attempting to breathe fire into the economy, it will help global growth. Europe, as well as the rest of Asia and Japan, relies greatly on Chinese trade and the moves in Beijing can only be good news for the flagging Eurozone.

US Economic Update – Hard luck for “Hard Landers”

But first… inflation! On Friday we got news that the Fed’s preferred inflation gauge, the core (PCE) price index, increased by 0.1% from the previous month. This measure, which excludes food and energy, rose at a 2.1% annualized rate over the past three months, aligning with the Fed’s inflation target.

The inflation announcement was pretty much in line with market expectations and we got a lukewarm reaction from the equity markets, with Dow up a bit, Nasdaq down and S&P 500 pretty much flat. Treasury yields and the dollar fell on expectations the figures will keep the Fed on track for more rate cuts in the coming months, while fuelling the ongoing debate over how big the reductions should be going forward. August inflation data showed broad cooling, with services prices excluding housing and energy rising 0.2% for a second consecutive month. Goods prices, excluding food and energy, fell by 0.2%, the largest decline in three months.

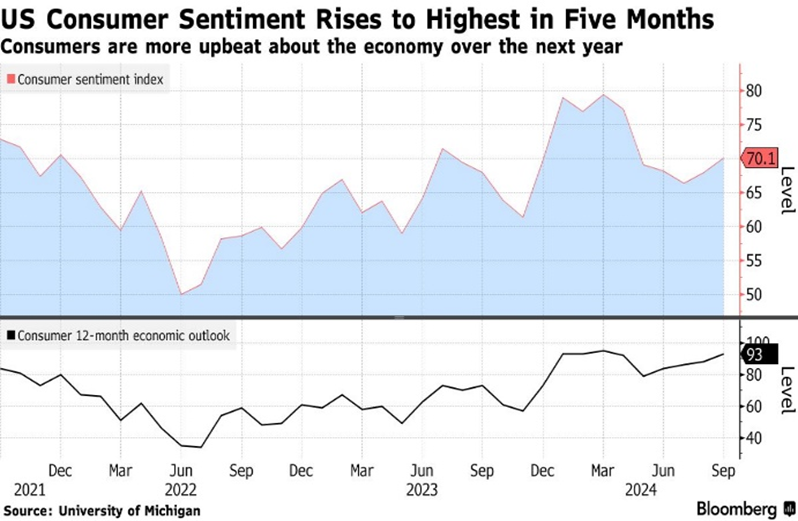

There was, however, a raft of economic data last week that will concern debt investors and delight the equity bulls and if markets hadn’t already been enjoying a good run, would have probably spurred to shares to a greater degree. We got a big uptick in consumer sentiment, which will probably be strengthening Kamala Harris’s hopes of entering the Whitehouse. The improvement to the index this month was probably driven by the 0.5% rate cut from the Federal Reserve, along with lower gas prices and ongoing strength in equity markets.

And we got more data supporting the Goldilocks Scenario, as after hitting a record low in July, pending home sales showed a slight increase in August, indicating that existing home sales may have stabilised. The recent drop-in mortgage rates in September will most likely help support a steady recovery in home sales, particularly in the fourth quarter of this year and into 2025.

But perhaps the biggest news of the week was the big upward revision to US GDP! Remember, in the long run it is GDP growth that leads to higher corporate earnings and provides the biggest driver of equity prices. I keep banging on about the fact, but I am convinced the US economy is in a much better place than many commentators would have you believe, so it was nice to get some ‘confirmation bias’.

The revisions reveal the US economy has been growing even stronger than previously thought. With upward adjustments to income and productivity, the numbers really do highlight solid foundations for the recovery. GDP was revised higher by over one percentage point, driven by increased consumer spending and business investment. Personal incomes and corporate profits were also revised upwards, closing the gap between GDP and gross domestic incomes. The revisions only strengthen my confidence that the economy will continue expanding, but it does leave all the expectations for significant rate cuts looking overdone. Good news for equities, less so bonds…

Political Shock in Japan spooks markets after close

Although the Japanese equity market closed off a good week higher on Friday, in afterhours trading it looked to be down as much as 6% (IG Index). The trigger, in a surprising turn of events, came when Japan’s ruling Liberal Democratic Party (LDP) made an unexpected choice for its new leader, and thus the next prime minister. The party could have picked Sanae Takaichi, potentially its first female leader and a follower of Shinzo Abe’s policies credited with helping Japan’s economy recover from stagnation. Alternatively, they could have chosen Shinjiro Koizumi, a young and charismatic figure. Instead, the LDP opted for Shigeru Ishiba, who has positioned himself as the opposite of Abe’s legacy.

Ishiba is known for his more independent, outsider stance within the party, advocating for a more balanced approach to diplomacy, particularly with China, which may create tension with the U.S. However, Ishiba’s unclear economic plans and opposition to “Abenomics” — the economic policies spearheaded by Abe — may lead to uncertainty. His rise comes as Japan’s political landscape shifts, with the opposition showing signs of becoming more organised, possibly challenging the LDP’s long-standing dominance. Public dissatisfaction, evident in plummeting approval ratings, led to Prime Minister Fumio Kishida stepping down, paving the way for Ishiba’s surprising victory.

Next Week…

All eyes will be on the US Employment Report (Friday, Oct 4). I am not exactly sure how markets would react to either a weaker or stronger jobs picture as we have re-entered the twilight zone again, where bad news could mean more rate cuts , which could be good news . And vice versa . It probably just comes down to sentiment, and which way investors choose to drive the markets . We also have Eurozone Inflation Data (Oct 3), where we might see continued weakening which could pave the way for more ECB cuts.

This content is intended for financial professionals only. These are the author’s views at the time of writing and may be subject to change. This content is not intended to provide the basis for any investment advice or recommendation. Any forecasts, figures, opinions, tools, strategies, data, or investment techniques are included for information purposes only.

The information presented is considered to be accurate at the time of production and has been obtained from or based upon sources believed by the author to be reliable and accurate, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Please visit our Regulatory Information and Terms of Use pages for more information.

Production

Production