Steady As She Goes…

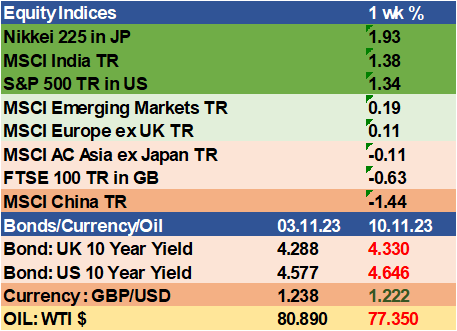

No great fireworks from the financial markets last week, which was encouraging after the drama of the week before. Japan, India and the US (after a strong final session) led gains, with other markets broadly flat to down. Yields headed a little higher but no great alarm bells.

Sterling weakened a touch, but the falls in oil continued with WTI breaking and staying below $80 a barrel. You will be relieved to hear, that as there were no major economic releases last week, and no new wars or pandemics to write about, this Market Matters is a quicker read!

UK

Probably the most relevant piece of information for our daily lives was the read we got on the state of our own economy, with the publication of the UK GDP figures, which pointed to a state of limbo. The UK’s GDP growth for September was 0.2% month-on-month, matching expectations and slightly outperforming consensus predictions. This growth marks the second consecutive monthly rise. However, a downward revision for August’s growth led to a stagnant economic performance over the three months to September, a decline from the 0.2% growth in Q2. The stagnation resulted from declines in consumer spending, government consumption, and business investment, though this was partially offset by a positive net trade contribution.

Digging in, as Q3 concluded, there were signs of economic momentum, including a potential reduction in industrial action, which previously affected public sector and transport output. This trend suggests a modest improvement in the economy for Q4. However, the broader view reveals minimal GDP expansion since early 2022, with a trend of near stagnation expected to continue into 2024.

Several challenges persist, including rising mortgage payments as homeowners move away from fixed-rate deals, high inflation, and signs of a weakening job market. Additionally, high corporate financing costs and economic uncertainty are hampering investment, while fiscal policy remains stringent. Despite these challenges, there are positive factors that may prevent a severe downturn in the short term and could lead to an upturn in growth from the second half of 2024. One such factor is the recent growth in real wages, expected to continue as inflation slows. Moreover, the higher interest rates are providing an income boost to savers. It may well stay the same for a while, but we are probably close to an inflection point where momentum could switch in either direction…

US

We got another chance to hear from J Powell last week, when he spoke at a panel organised by the IMF, and here he was at pains to stress that the Fed’s fight against inflation is far from over, and there will be more rate increases if the data suggests they are necessary. I think the increase in hawkish tone was most likely in response to the significant easing in financial conditions that had followed his November Fed press conference, since which, yields had fallen sharply and equities surged (probably a bit too much for their liking). His talk did temporarily halt the equity rally and send yields higher, although much of the move in bonds seems to be more likely caused by a disappointing Treasury auction, which had seen less demand than expected. Remember, that bond prices (like all goods and services) are set by the simple dynamic of demand meeting supply, and the seemingly unlimited demand for US treasuries should not be taken for granted.

Other releases last week included the ‘Atlanta Wage Growth Survey’, which suggested that wages are not dropping fast enough to give the Fed comfort. I am sure that the thing keeping J Powell up at night is the strength of the jobs market, as until this shows signs of loosening, he will be unable to categorically declare victory over inflation.

Earnings

We are just about at the end of the Q3 earnings season, with over 90% of companies having reported, and for the most part it has provided positive surprises. Over 80% of companies have reported ‘Earnings Per Share’ (EPS) above estimates and we went into this season with analysts expecting an overall year-on-year decline. It looks instead as if we will see YoY earnings growth of more than 4%. Expectations for the ongoing path have been updated and whilst Q4 2023 is likely to be a little weaker than Q3, as we go forward in to 2024, it looks like earnings are likely to pick up, helping ease the pressure on market valuations.

Whilst the last thing I want to do is tempt fate, with the prospect of higher earnings next year, the ingredients are still there for a ‘Santa rally’ in equities into year end, with people trying to bank next year’s possible gains in this year! There is also enough ‘worry’ in the market and cash in money market funds to keep market conditions healthy.

Production

Production