Navigating market turbulence, delivering consistent outcomes

Author: Paul Hogg, Head of distribution, 8AM Global

We launched the 8AM AQ Classic portfolios in June 2020 & what a five years it’s been…

The past five years have tested investors in ways few could have imagined. A global pandemic shut down the world. War returned to Europe. Inflation surged to multi-decade highs. Interest rates rose at the fastest pace in a generation. Along the way, we’ve endured political chaos, energy crises, a cost-of-living squeeze, conflict in the Middle East, and the return of tariffs as a dominant global risk.

Through it all, volatility has been constant, but so has our process.

The 8AM AQ Models were built for exactly this: to deliver robust, repeatable outcomes through thick and thin. Not just when markets cooperate, but especially when they don’t.

Five-Year Performance: Evidence, not opinion

From June 2020 to June 2025, the 8AM AQ Classic models have delivered strong, risk-adjusted returns:

AQ Classic 7: 59.98%

AQ Classic 6: 50.17%

AQ Classic 5: 42.23%

AQ Classic 4: 28.15%

AQ Classic 3: 17.19%

Each model has outperformed its Investment Association benchmark sector average by meaningful margins and have done so through an extraordinarily complex investment environment.

What’s more, it’s not just about portfolio performance, it’s how it’s been delivered: with clarity, consistency, and adaptability.

Out of interest, I thought I would see the effect of our AQ process in action – what would have happened if we hadn’t rebalanced and just left the initial fund selection alone. With relief, when I ran the 5 year screen of our live performance versus our original portfolios it shows that our outperformance versus sector has come from the added value of continuous fund optimisation, rebalancing and some measured (data-driven) tactical tilts!

And a reminder of how we work…

At the heart of AQ is a clear mission: to remove noise, reduce bias, and build investor performance on using data, not dogma. Every month, we scan the full Investment Association universe, creating clear relative rankings that form the foundation of our fund selection. It’s a system built to be responsive, consistent, and – above all – transparent.

The results speak for themselves:

- A 77.3% rolling 12-month fund selection win-rate versus sector averages

- Consistent outperformance versus benchmarks across every risk band

- A 0.15% management fee – one of the lowest in the market

AQ in numbers

Behind these great outcomes lie proportionate, adaptable portfolio conviction, concentration and turnover…

122 total holdings used since launch.

Comprising 91 equity funds, 22 fixed income, 4 absolute return, and 4 money market funds.

Typical number of portfolio holdings: 25

Lowest number number: 18

Highest number of positions: 32

Average equity fund holding period: 10.9 months.

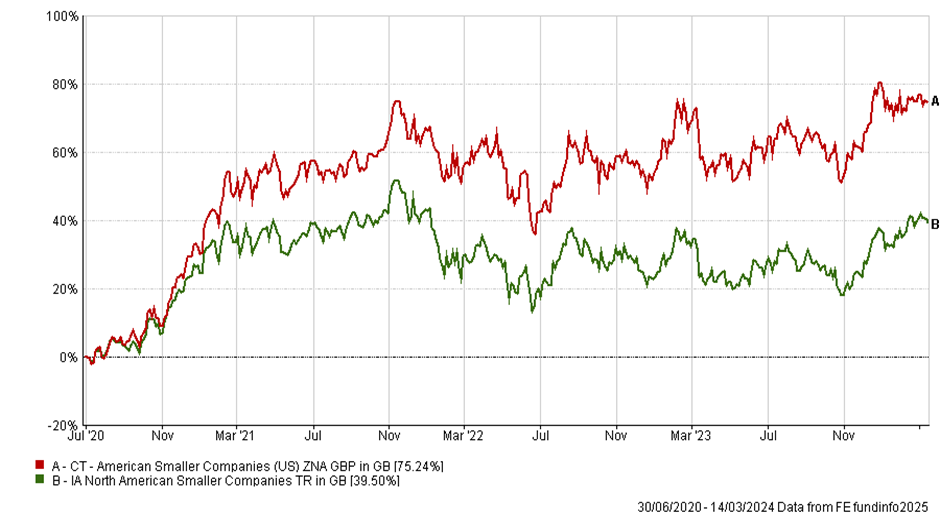

Longest-held active equity fund:

CT – American Smaller Companies, held for over – 44 months July 2020 to March 2024…

…another good example is Fidelity UK Smaller Companies – 24 months from Nov 22 to Sept 2024.

This blend of systematic conviction and discipline – holding winners and dispassionately cutting laggards – has helped us navigate regimes and cycles with confidence.

What worked, what changed?

The AQ journey started strong. Our early allocations to high-growth managers in 2020 paid off handsomely, with funds like Baillie Gifford American and Slater Growth deftly capturing the COVID recovery rally. We pivoted early in 2022, cutting exposure to rate-sensitive names as inflation surged. Arguably the shift to value and large cap could have been earlier, but we made it and especially via funds like Invesco UK Opportunities, Liontrust UK Growth – proved timely, as did our move to short-duration bonds in 2022 to protect capital during the rate shock.

In 2023, overweighting the US and retaining consistent technology exposure helped us ride the early stages of the AI-led rally. The portfolio’s core conviction in US equities, alongside selective global and thematic picks, helped performance remain resilient through the regional banking scare.

In 2025 we’ve rotated back into European equities and (more recently still) small cap more broadly, taking advantage of lower valuations and signs of positive momentum building.

One constant: we’ve always had a tech position in the mix to enable granular control over the thematic exposure globally (but most pragmatically in the US). While the Magnificent Seven stumbled in early 2024, their resurgence this year has reinforced the importance of retaining selective, proportionate exposure to innovation-led growth.

Where do we go from here?

The next five years will bring new surprises, we can be sure of that. Whilst the fundamental, systematic principles that underpin our process won’t change, we’ll continue to innovate and build on our research to ensure that our AQ portfolios (and our other products) remain agile and adaptive.

We don’t believe in trying to outguess the market or making emotive tactical bets. Instead, we anchor our assumptions to crowd sourced tactical asset data and seek alpha through disciplined fund selection. The gains can seem incremental year to year, but over time, the advantages of compound growth without significant tactical blunder builds real long term value.

Markets will fluctuate. Regimes will change. But process endures.

Data beats instinct.

Process beats prediction.

…and transparency builds trust.

Whatever the world throws at us next, we’ll be ready.

This content is intended for financial professionals only. These are the author’s views at the time of writing and may be subject to change. This content is not intended to provide the basis for any investment advice or recommendation. Any forecasts, figures, opinions, tools, strategies, data, or investment techniques are included for information purposes only.

The information presented is considered to be accurate at the time of production and has been obtained from or based upon sources believed by the author to be reliable and accurate, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Please visit our Regulatory Information and Terms of Use pages for more information.

Production

Production