When Egos Collide!

Author: Tom McGrath, Head of MPS, 8AM Global

Market Overview

It was always coming. A public bust-up between Trump and Musk felt inevitable. Two oversized egos with outsized platforms and zero impulse control. That the bromance lasted this long is the real surprise. The spark? Musk’s suggestion that Trump owed his political revival to billionaire backing. Trump hit back with fury, calling him ‘CRAZY’ and hinting at lost government contracts. Musk retaliated with a (veiled?) Epstein reference and threats to ground NASA missions. Markets flinched, Tesla fell 14%, and Musk personally lost $34 billion in a day. But the fight seems to have cooled almost as quickly as it flared. Both men have too much to lose. Trump needs Musk’s reach, as well as the financial support for Republicans, and Musk needs federal funding.

For now, it’s back to mutual tolerance, if not affection, and markets rallied on Friday, helped by a deflation in tensions between the two narcissists and a US jobs report that, on the surface, looked positive. So, as we sit nearly halfway through the year, it seems to be shaping up as another reasonable one for global equity markets. Even the US markets, in dollar terms, have remarkably clawed their way back to levels seen earlier in the year despite the macroeconomic underpinnings becoming more fragile.

It’s a peculiar kind of recovery that leaves me a little uneasy, more rooted in positioning and relative valuations than in conviction about growth or policy. Despite tepid earnings momentum, cooling demand, and the spectre of tariff-driven inflation, risk assets have bounced back. Volatility has faded, credit spreads have narrowed slightly, and equity benchmarks have shrugged off poor data with the detachment of a market that prefers the absence of bad news to the presence of good. Yet beneath the surface, many of the foundations that supported the bull rally since the end of 2022 have begun to erode. Consumer strength appears more selective than broad-based, business investment is slowing, and the global policy environment remains muddied by political uncertainties. The rebound is real, but I can’t help but think it rests on a shakier footing than the price action implies.

US

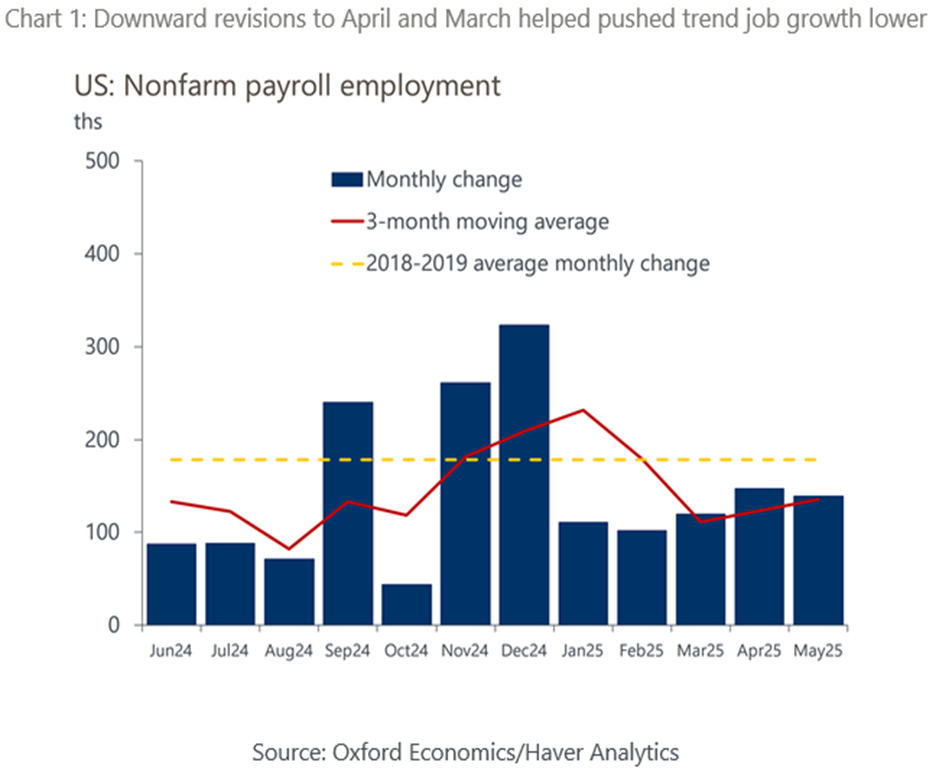

The May jobs report offered something for everyone, just not enough to change the Fed’s course. Headline nonfarm payrolls rose by 139,000, a touch above consensus, but downward revisions to the previous two months lopped off another 95,000 jobs. The unemployment rate held steady at 4.2%, and average hourly earnings rose by 0.4%, nudging annual wage growth to 3.9%. It’s not a report that screams recession, but neither does it suggest resilience. It’s what you’d expect in an economy beginning to feel the weight of higher borrowing costs, slower hiring, and creeping uncertainty around tariffs.

Under the surface, the story is more mixed. Job growth is becoming increasingly concentrated in healthcare and hospitality, with education and social services bearing the bulk of the workload. Outside those areas, momentum is softening. Retail, logistics and manufacturing all shed jobs in May, and the data on federal government employment continues to reflect the impact of hiring freezes rather than layoffs.

This gradual deceleration is precisely why the Fed is in no rush to act. There’s no clear sign that the labour market is unravelling, but equally, there’s no sense that inflation risks have receded. If anything, the tariff backdrop is tilting inflation expectations upward. The Fed knows the full cost of higher steel and aluminium duties, and the knock-on effects on supply chains haven’t yet filtered through. Why would you cut rates into that? Holding steady is not indecision; it’s discipline.

Trump, of course, sees it differently. His latest demand for a 100-basis-point cut would be laughable if it weren’t so dangerous. Asking the Fed to slash rates while layering on trade restrictions is like flooring the accelerator while yanking the handbrake. The market’s not buying it, and neither is the Fed. Powell’s refusal to entertain that line of thinking gives me hope. Fortunately, there is still an adult in charge of the national bank account. A cut in September remains a possibility if conditions weaken further and recent indicators have turned more cautious. The ISM manufacturing index has now declined for four straight months, and the services sector unexpectedly contracted in May. The Fed’s own ‘Beige Book’ noted rising concerns about tariffs and policy uncertainty, with businesses increasingly wary about future investment. Trade data tells a more nuanced story. Overall volumes have held up, but a clear shift is underway: imports from China are falling, while Vietnam and South Korea are picking up some of the slack, particularly in technology-related goods. The US economy is not stalling, but it is slowing. Consumer spending is holding up and the labour market still has momentum, but the direction of travel is clear.

Europe

If the Fed is paralysed by uncertainty, the European Central Bank continues to act. Last week’s decision to cut interest rates by 25 basis points, bringing the benchmark rate to 2%, was widely expected. What wasn’t expected was the tone. Christine Lagarde was quick to dampen expectations of a sustained easing cycle, describing the move as data-dependent and suggesting that rates may now stay on hold unless the inflation picture shifts decisively.

Markets took this as a classic hawkish cut: a move made not because growth is collapsing but because the ECB believes it has done enough. Eurozone inflation remains broadly in check, close to the 2% headline, but services prices are proving sticky, and wage growth is still brisk in several member states. The Governing Council’s messaging reflected a desire to ease cautiously without fuelling fresh concerns about overheating.

The market reaction was telling. Yields on German and French bonds rose, the euro strengthened, and equities held firm. While the rate cut itself was priced in, the accompanying confidence was not. It was seen less as a sign of fear and more as a signal that the ECB feels Europe is on firmer footing or at least firmer than the US at this stage.

It also helps that Europe, unlike the US, retains some fiscal headroom. Germany’s tentative return to fiscal stimulus has been well received, and the broader European story is increasingly about recovery and reform rather than overheating and repricing. European equities remain the best regional performers year-to-date, and the euro’s recent strength reflects a more fundamental reappraisal of the region’s stability and capital appeal. This isn’t just about a weaker dollar. It’s also about Europe doing relatively better.

China, Emerging Markets & Japan

I’ve been guilty of giving the Asian markets less coverage in these pages than they probably warrant. The drama emanating from the US, especially when Trump is involved, tends to dominate the narrative, and there’s a natural home bias that keeps the UK (and Europe, by extension) front and centre. But that doesn’t mean the rest of the world isn’t on my radar. Quietly and without much fanfare, several major Asian markets and the broader emerging market universe are showing signs of durable momentum.

China, after years of scepticism and underperformance, is finally showing signs of a sustainable recovery, not driven by state-mandated lending sprees or property speculation but by a more measured combination of consumer resilience, service sector strength, and targeted stimulus. The Q1 GDP figure surprised to the upside, with retail sales and travel spending suggesting the country’s long-awaited pivot to a consumption-led model might be more than just wishful policy thinking. Even amid slowing exports, domestic demand is doing some heavy lifting. Investors who had written off Chinese equities amid the regulatory crackdowns and geopolitical gloom are quietly reassessing their stance. Valuations remain depressed, global allocations are still low, and the policy mix, combined with steady credit conditions, mild fiscal easing, and currency stability, seems designed to entice rather than overwhelm. What might surprise you is that, over the past year, Chinese equities have returned significantly more than the US!

The broader Emerging Market (EM) complex is benefiting too. The declining dollar has given many EM central banks breathing space, with currencies stabilising and inflation pressures easing. As capital returns to risk assets, EM debt and equities are drawing attention, particularly in Asia and Latin America. Brazil and Mexico remain attractive for yield-seekers, while Korea, India, and Indonesia are emerging as the preferred growth stories. Supply chain diversification, the so-called ‘China+1’ trend, continues to favour regional players, particularly in tech and energy infrastructure. Meanwhile, lower commodity prices and a soft US dollar have reduced imported inflation, improving real incomes across several EM economies.

Japan stands out as a case of long-delayed promise meeting reality. For decades, the market has flirted with international interest before retreating into obscurity, but this time may be different. Corporate governance reforms are gaining traction, shareholder returns are improving, and inflation (finally) is no longer purely theoretical. Wage gains are materialising, nominal GDP is rising, and for the first time since 2007, the BoJ is lifting interest rates. That doesn’t mean aggressive tightening is coming, far from it, but the end of negative rates suggests that the patient has come off life support. The yen remains weak, exports are steady, and domestic demand is finally playing a more meaningful role.

For investors, the implications are quietly optimistic. Corporate earnings are trending higher, with profit growth expected to remain solid into 2026, helped by both structural reform and a more shareholder-friendly stance from Japanese firms. Buyback activity has accelerated, margins are expanding in key sectors such as banking and automation, and the backdrop of mild inflation with favourable real rates is constructive for equities. For now, Japan offers one of the few developed markets combining monetary normalisation with genuine earnings momentum. After years of underperformance, it’s a market that could turn promise into performance, but that would need further calm on the tariff front.

What links all three stories, China, EM, and Japan, is that they are no longer purely tactical trades. They are part of a broader structural shift in capital allocation. As the US faces higher political and fiscal risk and Europe navigates its slow-burning reforms, the gravitational pull toward Asia is strengthening. Not without risk, but with valuations, demographics, and geopolitics now pulling in their favour after years on the sidelines, the periphery of many portfolios may yet become the core.

UK & European Small Caps are on the rise!

And finally, something unusual is stirring in UK and European small caps. After years in the macro-driven wilderness, they’re beginning to outperform their large-cap peers.

This story has been regurgitated by smaller-cap fund managers for quite a while now: “Both relative to history and to large caps, smaller companies in the UK have never been cheaper”. So what? I hear the cry from many investors who have been burnt chasing the elusive small-cap bounce. But, we now have a domestic economy that has begun to surprise to the upside, a consumer with very healthy savings and a central bank cutting rates. Throw in the rising tide of deal-making and M&A activity across UK small caps, with takeover premiums running close to 50% in some cases. That is a more positive vote of confidence that value still lies beneath the surface. Europe tells a similar story. Softer inflation and a dovish ECB are creating a more supportive backdrop for smaller, more cyclical companies that were largely ignored during the rate-hiking cycle.

Valuations remain cheap, positioning is light, and the macro is no longer outright hostile. After years of silence, small and mid-caps are finally starting to make some noise.

This week…

It is a crucial week for markets as US CPI (Wednesday) and the Fed meeting collide. Inflation is expected to cool slightly, but any upside surprise could disrupt expectations for a September cut. The Fed won’t move rates, but Powell’s tone and the dot plot will matter.

In Europe, post-cut ECB commentary will help clarify how far Lagarde is willing to go, while in the UK, labour data (Tuesday) and monthly GDP (Wednesday) could swing the case for an August BoE cut.

On the corporate side, Oracle and Adobe report in the US, with Inditex offering a key read on European consumer demand. The G7 summit in Italy may add geopolitical spice, with trade and tariffs back in the spotlight.

This content is intended for financial professionals only. These are the author’s views at the time of writing and may be subject to change. This content is not intended to provide the basis for any investment advice or recommendation. Any forecasts, figures, opinions, tools, strategies, data, or investment techniques are included for information purposes only.

The information presented is considered to be accurate at the time of production and has been obtained from or based upon sources believed by the author to be reliable and accurate, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Please visit our Regulatory Information and Terms of Use pages for more information.

Production

Production