From FOMO to FEMO

Authors: Tom McGrath, CIO & Ash Weston, Head of MPS

US markets entered the second half of the year on a firm footing despite a holiday-shortened trading week leading into America’s 250th Independence Day celebrations. Trading volumes were naturally lighter ahead of the long weekend, but investors still had plenty to digest. The S&P 500 continued its advance and is now up around 9% year-to-date in USD terms, the Dow Jones Industrial Average reached fresh record highs, and the Nasdaq remained close to its own highs despite some late weakness in parts of the semiconductor complex.

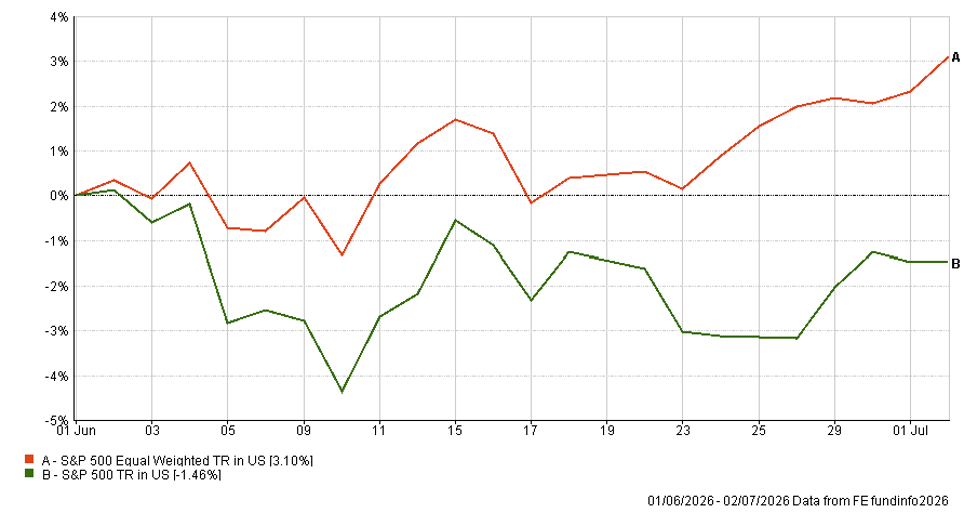

Encouragingly, leadership continued to broaden beyond the largest technology names. Financials, industrials and healthcare all performed well; small and mid-cap companies continued to participate, and the equal-weight S&P 500 outperformed its market-cap-weighted counterpart (as it has since the start of June).

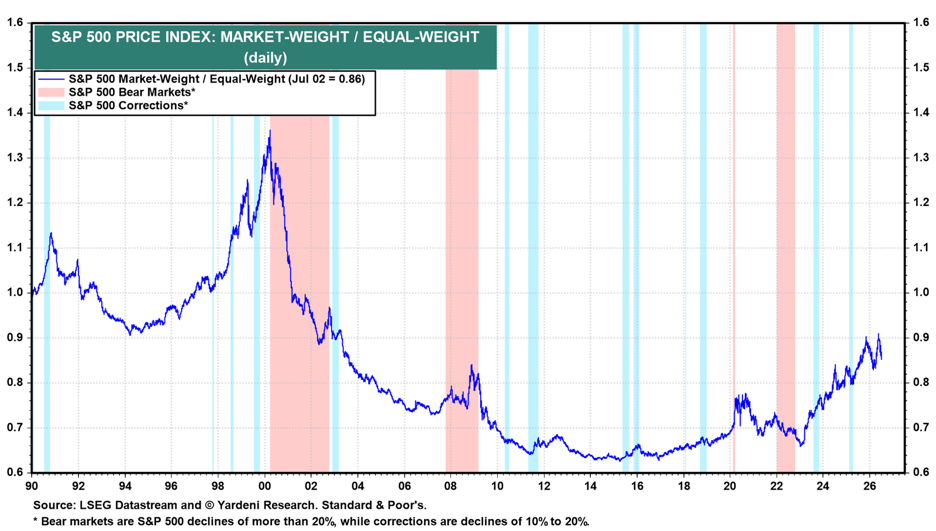

This outperformance should, however, be couched in the long-term behavior of the market-cap US index relative to its equal-weight index. Pulling back during bear markets, but generally trending upwards towards Market Cap. Note that the disconnect between market-cap concentration and Equal-weight is not yet as pronounced as in the dotcom era, given that we are hovering just below 1994 levels.

Away from equities, Treasury yields were relatively stable as investors balanced a softer labour market against continued Federal Reserve caution. Oil prices drifted lower despite ongoing tensions in the Middle East, reflecting the market’s belief that global energy supplies remain largely unaffected.

Overall, it was another week that reinforced the resilience of risk assets despite an increasingly noisy geopolitical and political backdrop. The story of this bull market is beginning to evolve. For much of the past two years, investors have focused on three themes: artificial intelligence, disinflation and surprisingly resilient economic growth. Those foundations remain firmly in place, but the debate is becoming more sophisticated. Investors are no longer asking whether AI will transform the global economy. They are asking where the long-term profits will accrue, whether current investment levels can be sustained and whether expectations have become too ambitious. Those are healthy questions for a maturing bull market rather than evidence that it is coming to an end.

From FOMO to FEMO

Yardeni’s latest note captures the distinction neatly. The late-1990s technology bubble was driven largely by FOMO: investors paying ever-higher multiples for businesses with limited profits and often little visibility on future cash flows. Today’s market is better described as FEMO: Fabulous Earnings Momentum. The largest technology companies are highly profitable, cash-generative, and balance-sheet-strong. That does not mean there is no excess, but it does mean the excess is showing up elsewhere.

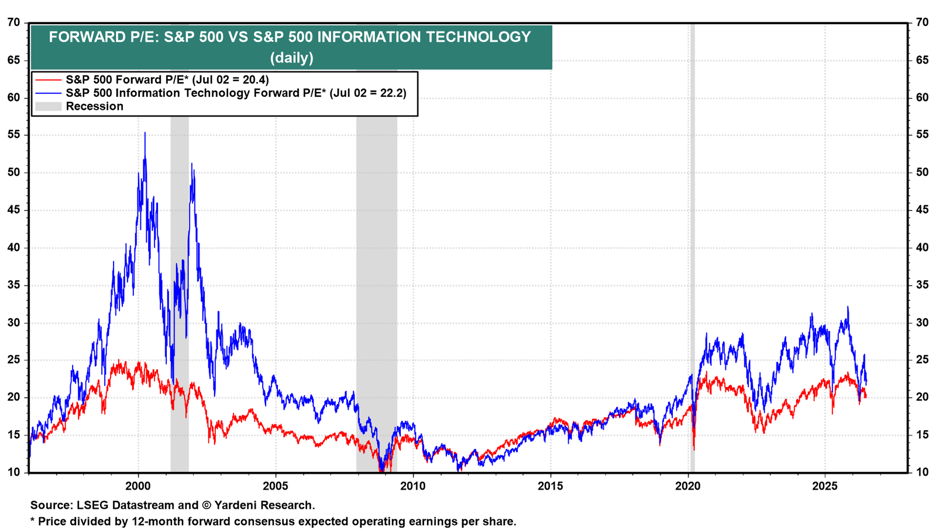

Scale is important here – the two charts highlight the key differences. First, the extreme range of forward P/E in the US IT sector compared to the broader S&P around the dotcom bubble compared to now.

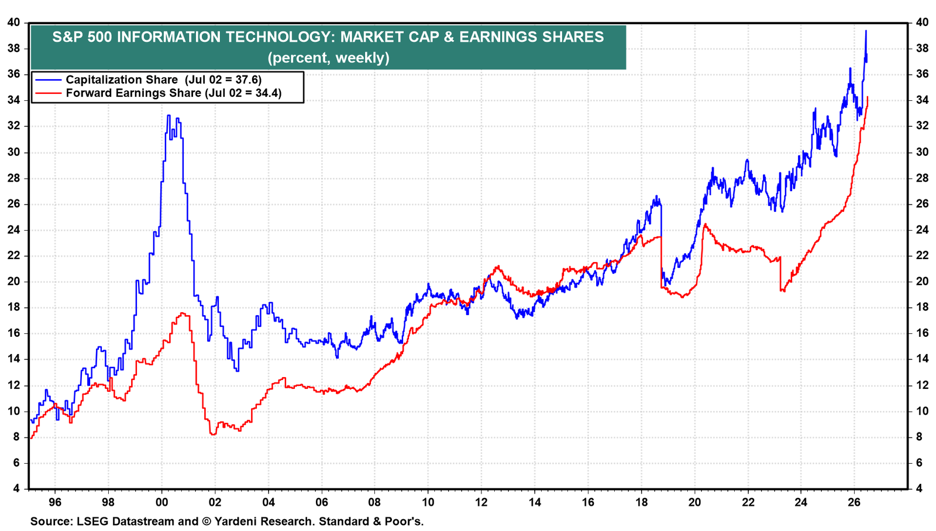

And around the dotcom crash, market cap and share price ran far ahead of the forward EPS, whereas this market appears to move in lockstep and has been led by EPS; hence, FEMO rather than FOMO.

We remain unconvinced by comparisons with the technology boom of the late 1990s. Noting that the current forward P/E of the S&P 500 Information Technology sector is roughly 22 times, not dramatically above the wider S&P 500, compared with a peak of around 55 times before the early-2000s tech wreck. That is not a trivial difference. Today investors are not generally paying fantasy multiples for businesses with no earnings. They are paying full prices for companies that are already producing exceptional profits.

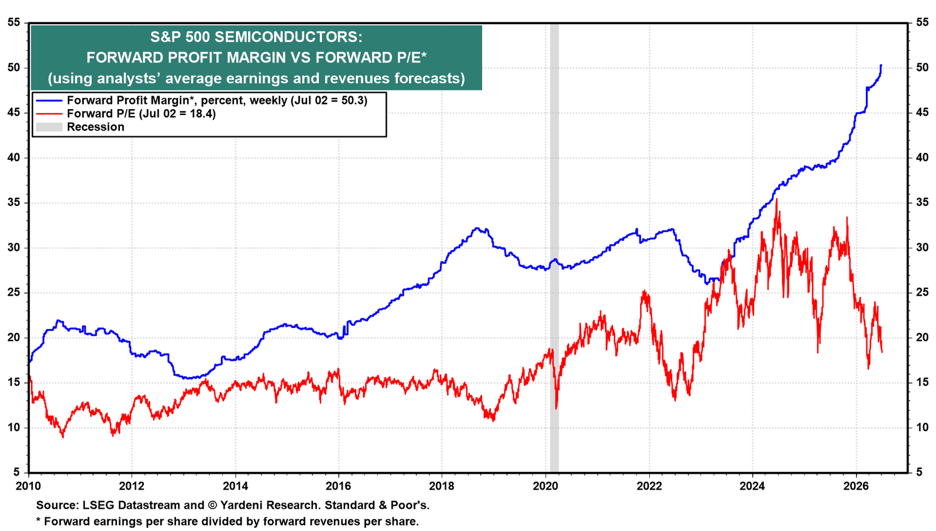

The more plausible bubble risk lies in earnings expectations rather than valuation multiples. Analysts have lifted long-term earnings growth expectations for the S&P 500 to record levels, with technology assumptions particularly high. Semiconductor expectations are the obvious pressure point. The chart below highlights that the forward profit margin for the S&P 500 Semiconductors industry has risen to a record level, above 50%. That may ultimately prove justified if AI demand remains extraordinary and supply remains constrained, but it leaves much less room for disappointment than it did a year ago.

Remember, the AI trade does not need to be completely hollow to disappoint. It merely needs expectations to have moved too far ahead of reality. Falling inference costs, rising competition from China, and the relentless pace of innovation have prompted investors to reassess the durability of today’s earnings forecasts. Expensive chips can quickly become obsolete in a market where the next generation is always around the corner.

The hyperscalers continue to commit hundreds of billions of dollars to AI infrastructure. Still, investors increasingly want evidence that these investments will generate attractive returns rather than simply ever-larger capital expenditure budgets. Twelve months ago, almost any announcement involving AI attracted a positive reaction. Today, investors want measurable improvements in productivity, revenue growth and profitability. That is not a bearish development. It is the natural evolution from exciting new story to sorting the winners from the losers.

Earnings remain the ballast

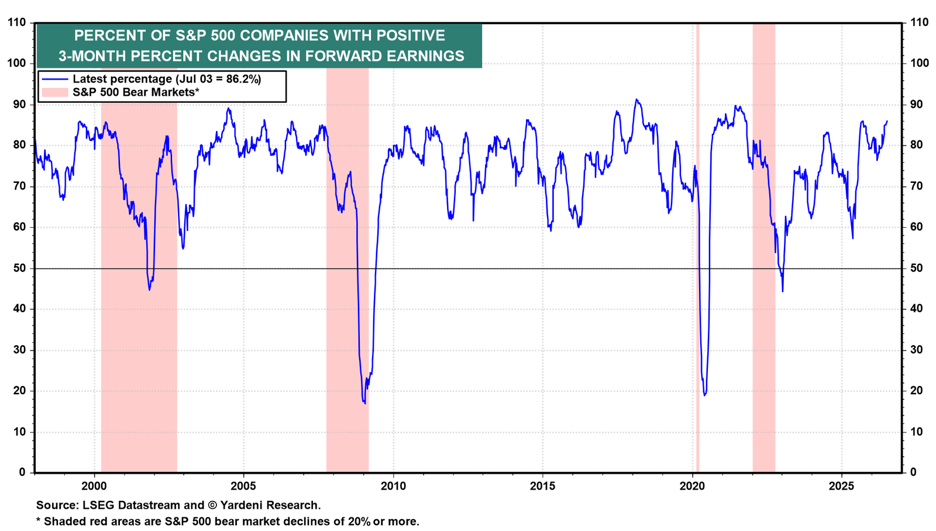

The reason we remain constructive is that the earnings backdrop still looks supportive. Yardeni’s data show S&P 500 forward earnings reaching a new record high at the end of June, with analysts projecting strong growth this year and next. More importantly, the improvement is no longer confined solely to the largest technology names. The share of S&P 500 companies reporting positive three-month changes in forward earnings has risen to a new cyclical high, precisely the kind of breadth investors should want to see at this stage of the cycle.

That does not mean markets are cheap. They are not. Nor does it mean every earnings forecast will be achieved. Expectations are now high, particularly in the AI supply chain. But there is a meaningful difference between a valuation-led speculative excess and an earnings-led bull market in which investors demand proof. The former usually ends badly when liquidity turns. The latter can continue for longer than feels comfortable, provided earnings broaden, and policy does not become a renewed headwind.

This has been a recurring theme in recent weekly updates. The market has been working through an AI wobble, but that wobble has looked more like rotation than retreat. We are moving from a phase where AI adjacency was enough to one where capital discipline, margins, and end demand matter again. That is a healthier market structure, even if it feels less exciting than the narrow leadership of the last two years.

Rotation continues to strengthen the market

Perhaps the most encouraging feature of recent weeks has been the continued broadening of market leadership. At the start of the year, concerns centred on the extraordinary concentration of returns within the Magnificent Seven. More recently, performance has improved considerably. While the largest technology companies have recovered some momentum after their spring consolidation, leadership is increasingly being shared across a wider range of sectors.

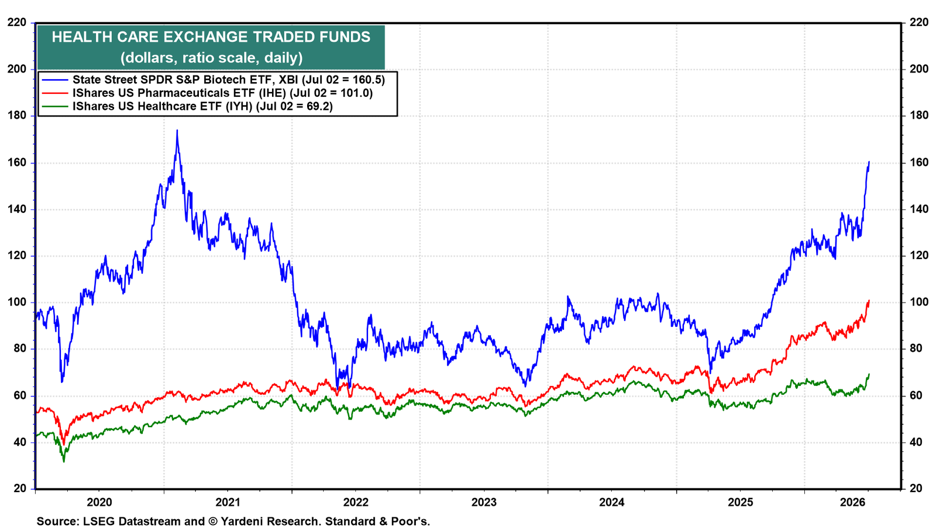

Banks continue to benefit from relatively healthy credit conditions and stable interest rates. Industrials remain supported by infrastructure spending, reshoring and AI-related capital expenditure. Healthcare has quietly begun to outperform after a long period of neglect, while cybersecurity has shown renewed signs of life after spending much of the past year in the shadows. Investors experiencing AI fatigue are increasingly finding comfort in businesses with more conventional earnings models and clearer near-term cash flows – as you can see below from the recent boost to Healthcare and Biotech.

Small and mid-cap companies have also continued to improve. Historically, sustained participation from smaller companies has been one of the more encouraging features of longer-lasting bull markets. Rather than relying on a handful of mega-cap technology stocks, investors are increasingly finding opportunities across a broader range of industries. The Russell 2000 making new highs and the equal-weight S&P 500 outperforming the cap-weighted index both point in the same direction: this rally is broadening, not narrowing.

Asia provides an interesting illustration of this transition. South Korea experienced renewed volatility as semiconductor shares corrected sharply before recovering, underlining just how crowded parts of the AI supply chain have become. Japan continues to benefit from corporate governance reform and improving profitability, while China remains a more mixed picture, balancing policy support against ongoing structural challenges in property and domestic demand.

The labour market remains the key macro variable

Economic data broadly reinforced the soft-landing narrative. The latest US employment report pointed to a further moderation in hiring while unemployment remained relatively low. Wage growth continues to cool gradually, and labour demand is easing without the kind of rapid deterioration normally associated with recession.

From a market perspective, this remains close to the ideal outcome. Inflation pressures continue to moderate while the economy appears sufficiently resilient to support corporate earnings. A cooling labour market is not automatically bad news for equities if it comes alongside improving productivity and stable margins. Indeed, one of the more important developments over the past year has been the evidence that the US economy is generating more output with fewer incremental hours worked. That is exactly the kind of productivity story that helps explain why earnings have remained resilient despite softer hiring.

Attention also remains focused on Federal Reserve Chair Kevin Warsh. His recent comments have underlined the Fed’s determination to maintain credibility on inflation even as labour market conditions soften. Investors are increasingly accepting that the Federal Reserve is unlikely to ride to the rescue at the first sign of equity market weakness. Monetary policy remains restrictive, but importantly it also appears increasingly predictable.

The stability in Treasury yields during recent weeks suggests investors are becoming more comfortable with that outlook. This matters. If yields remain range-bound, the broadening trade has room to continue. Banks, industrials, smaller companies and selective cyclicals can all live with a stable cost of capital. If yields were to spike, that would put immediate pressure back on equity valuations and risk appetite. For now, however, the bond market is not sending a distress signal. It is simply asking equities to justify themselves through earnings rather than multiple expansion.

Geopolitics remains a background risk rather than the main driver

The situation surrounding Iran and the Strait of Hormuz continues to deserve careful attention, but markets are still separating political rhetoric from economic reality. Oil prices remain relatively subdued despite continuing military tensions, suggesting investors see little evidence of meaningful disruption to global energy supplies. Shipping flows remain broadly normal, insurance markets have remained orderly and European gas prices have yet to signal any material deterioration.

As we have argued previously, the practical indicators are far more important than the headlines. Tanker movements through Hormuz, shipping insurance premiums, LNG exports and energy prices provide a much better guide to the economic impact than political statements alone. For now, markets appear comfortable with the view that geopolitical risks remain significant but contained. That could change quickly, but at this stage geopolitics is influencing risk premia rather than driving the macro cycle.

UK and Europe: value, politics and patience

Politics has also become a more prominent consideration for investors. In the UK, speculation surrounding Labour’s future direction, including increased discussion around Andy Burnham’s longer-term leadership prospects, serves as a reminder that political uncertainty can gradually influence business confidence even when immediate policy changes remain unlikely. The issue for markets is less the identity of any single politician and more the policy mix that ultimately emerges: taxation, spending discipline, regulation and the credibility of the fiscal framework.

The UK equity market continues to offer a more nuanced story than the domestic economy. Growth remains uninspiring, household confidence is fragile, and the gilt market remains sensitive to any sign of fiscal slippage. Yet UK equities retain several supports: low valuations, overseas earnings, dividend income, buybacks and ongoing takeover interest. The FTSE 100 does not need the UK economy to be exciting to perform reasonably well. Domestic mid and small caps, however, still need a calmer gilt market and clearer pro-growth signals if they are to unlock more sustained upside.

Across Europe, inflation continues to edge lower while growth remains modest but resilient. The region is unlikely to become the engine of global growth, but it increasingly appears capable of avoiding the recession many feared only eighteen months ago. Banks, defence, infrastructure, and selected industrials continue to offer support. Europe remains a market of dispersion rather than a broad-beta market, but that is not necessarily a bad environment for active investors.

Asia: AI strength, China questions and Japan’s reform story

Across Asia, investors continue to balance enthusiasm around AI investment with ongoing concerns surrounding China’s economic recovery. Korea’s recent volatility highlights how quickly leadership can rotate within technology, particularly when expectations are elevated. Taiwan and Korea remain central to the global AI supply chain, but the market is increasingly distinguishing between structural winners and cyclical beneficiaries.

Japan continues to provide one of the more encouraging structural stories globally. Corporate governance reform, better capital discipline and improving profitability remain important supports, even if currency moves and policy normalisation will still create periodic volatility. China is more complicated. Policy support remains in place; valuations are not demanding, and selected technology areas continue to attract interest, but domestic demand and property remain unresolved constraints. For global investors, Asia still offers important diversification, but selectivity is essential.

This week(ish)…

Attention now turns to the start of the second-quarter earnings season, with the major US banks once again setting the tone. JPMorgan and Goldman Sachs report on 14 July, alongside the June CPI release, making this an unusually important morning for both earnings and macro sentiment. Expectations remain high. Strong results are likely to be rewarded, but any signs that profit growth is beginning to disappoint may be punished more quickly than earlier in the year.

Investors will also monitor Federal Reserve communications, inflation expectations and Treasury yields for confirmation that the soft-landing narrative remains intact. FOMC minutes are due this week, followed by CPI and the Beige Book next week, ahead of the Fed’s 28–29 July meeting. Any further evidence that inflation is easing without a meaningful deterioration in employment would remain supportive for risk assets. A stable yield backdrop would also help sustain the rotation into financials, industrials, healthcare and smaller companies.

Elsewhere, we will continue to watch developments in the Middle East through the lens of energy markets rather than headlines. Oil and LNG flows, shipping activity through the Strait of Hormuz and insurance costs remain more important for investors than political rhetoric alone. At the same time, market breadth remains a key test. Sustained participation from banks, industrials, healthcare, cybersecurity and smaller companies would reinforce the view that this remains a durable bull market rather than one dependent on an ever-narrower group of technology stocks.

The upcoming phase of this bull market may not align perfectly with the previous one, and that’s an important consideration. It is likely that this will require greater effort and insight, which creates opportunities for active investors to add greater value.

This content is intended for financial professionals only. These are the author’s views at the time of writing and may be subject to change. This content is not intended to provide the basis for any investment advice or recommendation. Any forecasts, figures, opinions, tools, strategies, data, or investment techniques are included for information purposes only.

The information presented is considered to be accurate at the time of production and has been obtained from or based upon sources believed by the author to be reliable and accurate, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Please visit our Regulatory Information and Terms of Use pages for more information.

Production

Production