Markets get ahead of themselves

Author: Tom McGrath, CIO, 8AM Global Ltd

After a deeply unsettled March and a remarkable recovery in April, markets look set to start the new week on a weaker footing after weekend developments around the Strait of Hormuz revived fears that the path to peace may be more fragile than last week’s rally implied. With shipping reportedly close to a standstill again, oil is likely to open higher and equities lower as investors reassess how quickly the Middle East risk premium can really be unwound. Even so, this does not necessarily mean that the broader move toward de-escalation has failed. President Trump still appears highly motivated to wrap up the conflict, and that raises the likelihood of another diplomatic push to get the Strait functioning again and keep the wider peace process on track.

That balance is important because the recovery in risk assets has become increasingly confident. Markets were no longer simply bouncing from oversold levels. They were beginning to price a broader muddle-through outcome in which de-escalation held, energy disruption eased, and strong earnings did the rest. That view may still prove broadly right, but the weekend has been a reminder that the process is unlikely to be smooth. If Hormuz remains disrupted, even temporarily, the optimistic move in equities and the sharp fall in oil seen late last week will look as though they ran ahead of events.

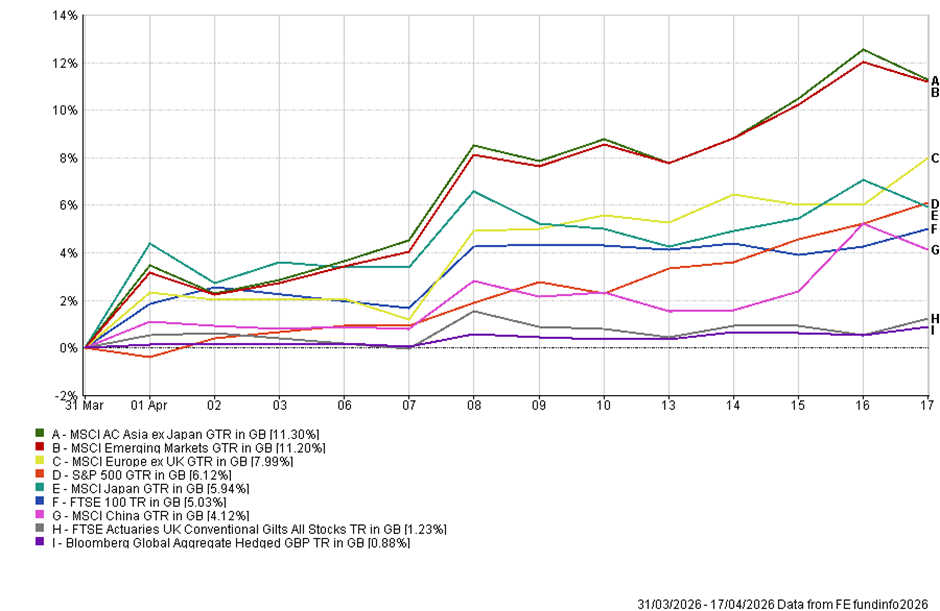

That said, the April recovery has still been impressive and, importantly, broader than many would have expected at the end of March. Asia ex-Japan has led the rebound, with emerging markets following closely behind, and Japan and Europe have also recovered strongly. The US has, of course, participated, but this no longer feels like a narrow rally driven solely by the old leadership. It looks more like a market increasingly willing to rebuild risk exposure across regions and sectors, helped by a better earnings backdrop and by the sense that, despite all the noise, the worst-case geopolitical scenario is becoming less likely. Positioning has clearly played a part, with many investors becoming too defensive at the March lows.

Still, the move has also had enough fundamental support to look more credible than a simple ‘short-covering’ rally. Investors have been encouraged by lower oil prices, a more conciliatory political tone from Washington and, increasingly, by earnings good enough to justify the recovery rather than undermine it.

The political dimension remains central. My reading is still that Trump wants out. The war has become more awkward domestically, particularly as fuel prices rise and the midterms approach. There is every incentive for The White House to declare progress, bank whatever concessions it can point to, and move back onto the domestic agenda. That does not mean all the hard issues have been solved. The details of any final settlement still look murky, and there are clearly major disagreements left over nuclear material, sanctions, and the precise terms under which Hormuz would operate. But it does mean Washington has a strong bias toward de-escalation, and that still matters a great deal for markets. The latest setback may therefore prove to be just that: a setback within a wider push to keep the diplomatic process alive.

That makes the split between equities and bonds even more interesting. Equities had been pricing the exit. Bonds, by contrast, were always more focused on the after-effects. Fixed income has actually held up reasonably well in April, which is reassuring, but it has never shown the same level of enthusiasm as equities. The reason is straightforward. Even if the immediate war shock fades, the inflationary consequences may linger. Higher energy costs, shipping disruption and pressure on food and input prices can still take time to feed through. The bond market has therefore been much less willing to assume that everything snaps back into place. The inflationary risk now is less about the first-round energy move, which markets can clearly see, and more about whether secondary effects begin to show up over the coming months. If oil remains elevated or if Hormuz disruption proves prolonged, today’s energy shock could still become tomorrow’s transport, food and broader services inflation problem. That is one reason the rates market has remained much less relaxed than the equities market. It is not that bonds are predicting disaster, but that they are less willing to assume the cleanest possible outcome.

US Earnings

The encouraging counterweight has been earnings. Early first-quarter reporting in the US has been good, and importantly, the first major bank results have helped validate the market’s optimism rather than challenge it. Most of the large US banks delivered solid numbers, with trading activity, capital markets revenue and stable operating performance helping the sector beat expectations. That matters not just because banks are important in their own right, but because they offer an early read on market conditions, credit quality, deal activity and confidence. So far, the message is not one of stress. Markets are not simply looking through bad news for the sake of it. They are looking at a conflict that still appears more likely to cool than re-escalate, an economy that has not yet shown signs of serious deterioration, and a corporate sector that is still producing healthy profits. That does not make the rally risk-free, nor does it remove the possibility that oil or inflation becomes a bigger problem again. But it does help explain why investors have been so willing to buy back into risk assets so quickly.

Technology remains an important part of that story. The upbeat TSMC numbers last week were a timely reminder that, amid the geopolitical volatility, one of the market’s most important structural growth themes remains intact. The AI build-out continues, demand for advanced chips remains strong, and the infrastructure side of that trade still looks robust. That does not mean all software and growth are suddenly fixed, but it does reinforce the idea that the market is not relying solely on geopolitics to return to highs.

UK

The narrative here is more mixed, though not without some positives. The better-than-expected February GDP number was a useful reminder that the economy entered the Iran shock in slightly better shape than feared. Services, production and construction all expanded, and taken together, that suggests first-quarter growth may still look respectable overall. In that sense, the UK was not already in obvious trouble going into the conflict. The problem is that the outlook has become more awkward since. Higher energy costs, slowing confidence, and renewed inflationary pressures all point to a tougher period ahead.

Europe

Remains more obviously vulnerable. The growth pulse is weaker, energy sensitivity is higher, and the region still looks more exposed to any prolonged inflationary aftershock. European equities have nevertheless participated strongly in the recovery, which makes sense given how pessimistically they had been priced at the March lows. But structurally, the region still feels less comfortable than the US and, in some respects, less flexible than parts of Asia.

Asia and Emerging markets

Have arguably been the most impressive part of the April rebound. That is partly because they were sold hard in March, but it also reflects the fact that earnings and valuation support in a number of those markets remained better than sentiment allowed. Japan has bounced well, emerging markets have recovered strongly, and China has shown more life than looked likely a fortnight ago. That broadening is one of the healthier aspects of the current move.

So, the broad message this week is still moderately constructive, but with a more obvious note of caution than there was on Friday. Markets have recovered far more quickly than many would have expected at the end of March, and the rebound has broadened out healthily. The White House still appears to want de-escalation, oil has come down from the highs, and the first phase of earnings season has been supportive. At the same time, the weekend has shown that the path to peace remains fragile, that energy disruption can return quickly to the forefront and that the macro clean-up has only just begun.

This week…

The Middle East moves straight back to the centre of the market story. Last week’s strong start to earnings season, particularly from US banks, was enough to validate a more constructive view while oil fell and ceasefire optimism built. But if Hormuz remains disrupted, markets will have to weigh those reassuring corporate signals against renewed pressure from energy prices and supply chains. That leaves this week’s heavier run of earnings even more important. Tesla, Boeing, Intel and Procter & Gamble are among the more prominent names due to report, alongside a much broader sweep of S&P 500 companies. Investors will want confirmation that profits remain resilient, but they may not be willing to reward good numbers in the same way if the oil market is moving the wrong way at the same time. After such a strong rebound from the March lows, markets look more vulnerable to disappointment than they did even a few days ago.

This content is intended for financial professionals only. These are the author’s views at the time of writing and may be subject to change. This content is not intended to provide the basis for any investment advice or recommendation. Any forecasts, figures, opinions, tools, strategies, data, or investment techniques are included for information purposes only.

The information presented is considered to be accurate at the time of production and has been obtained from or based upon sources believed by the author to be reliable and accurate, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Please visit our Regulatory Information and Terms of Use pages for more information.

Production

Production