A relief rally at last, but what has actually changed?

Author: Tom McGrath, CIO, 8AM Global Ltd

After a bruising end to March, markets finally managed a positive week over the Easter period, with a broad rebound across developed equities. The FTSE 100 led the move higher, Europe followed closely, and the US also recovered, while bonds were modestly firmer. It was a welcome shift in tone after several weeks dominated by geopolitical stress and rising energy prices, but the nature of the move is important. This did not feel like a clean turn in fundamentals. It was much more a relief rally, driven by a temporary easing in immediate fears and a sense that, even at this late stage, the Iran conflict might still be steered toward some form of negotiated pause.

Reports that US allies, including Pakistan, Egypt and Turkey, were pushing for a ceasefire, combined with repeated extensions to President Trump’s deadline for Iran to reopen the Strait of Hormuz, gave investors enough hope to believe that diplomacy had not yet failed. That alone was sufficient to trigger a rebound, particularly given how stretched positioning had become after the sharp drawdown into quarter-end.

The market reaction was consistent with that interpretation, with the strongest gains coming in regions that had been under the most pressure in recent weeks, while more structurally challenged areas showed less follow-through.

It is important not to imply that much has materially changed. The underlying situation remains highly unstable. Shipping through Hormuz is still running at a fraction of normal levels, oil prices remain elevated around $110, and attacks on energy infrastructure across the region continue. President Trump’s rhetoric has hardened again, with a clear escalation risk tied to Tuesday’s latest deadline. In that context, last week’s rally looks less like a durable re-pricing of peace and more like a temporary reduction in immediate panic. Markets bounced because the path to de-escalation remains open, not because the conflict has been resolved.

US Jobs

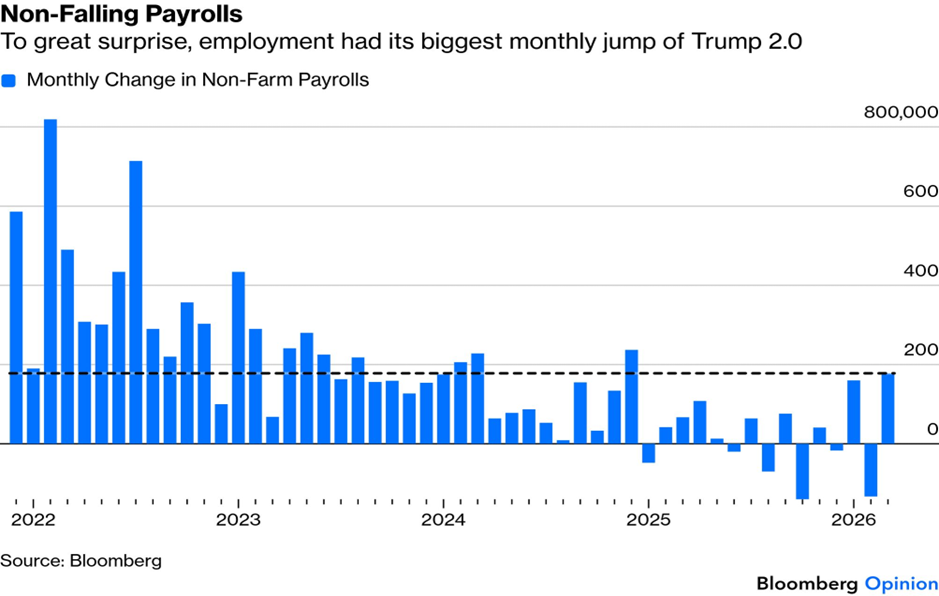

Alongside geopolitics, the other key support for markets came from the US economic data. The March non-farm payrolls report was notably stronger than expected, with job creation running at 178,000 and unemployment edging lower. At face value, that reinforces the idea that the US economy entered this shock from a position of reasonable strength, and that a near-term recession is not imminent. Survey data also continues to point to expansion in global manufacturing rather than contraction, adding to the sense that underlying activity remains intact despite the backdrop.

There are, however, reasons to treat the data with some caution. Labour market indicators have become more volatile and prone to revision, while other measures such as wage growth, hiring rates and job openings suggest a gradual cooling rather than any meaningful re-acceleration. The average duration of unemployment is also creeping higher, pointing to a labour market that is becoming more static as businesses wait for clarity on both trade and geopolitical risks. The message is that the US economy is stable, but not immune to external pressure, for example…

A prolonged period of elevated energy prices would still be expected to feed through into weaker consumption, particularly as higher fuel costs crowd out discretionary spending. With US gasoline prices now back above $4 per gallon, that transmission mechanism is already beginning to build. The risk is not an immediate downturn, but a gradual erosion of demand if current conditions persist.

Europe and the UK

The picture hereremains more challenging. Both regions are more directly exposed to the inflationary impact of higher energy prices, with less underlying growth momentum to absorb the shock. Recent data points to rising input costs and renewed pressure on corporate pricing, even as demand conditions soften. Central banks, particularly the BoE, appear increasingly aware of this trade-off, caught between higher near-term inflation and rising downside risks to growth and employment over time. The sequencing remains consistent with our broader framework, with inflation pressures appearing first and growth risks building more gradually underneath.

One notable counterpoint to the more cautious macro backdrop is that corporate activity remains relatively resilient. Global dealmaking has started the year strongly, with transaction volumes running ahead of last year despite the conflict. That suggests that, beneath the surface volatility, companies and private equity investors continue to position for longer-term opportunities. There are, however, early signs of hesitation, with deal activity slowing since the conflict began as financing costs rise and uncertainty increases. As ever, confidence is pivotal.

The key takeaway from last week is that markets remain highly sensitive to even small shifts in the perceived trajectory of the war. The rally showed how quickly sentiment can improve when a diplomatic path appears plausible, but equally, the tone at the start of this week, with firmer oil, weaker futures and renewed escalation rhetoric, highlights how fragile that improvement remains. In the near term, developments in the Middle East will continue to dominate, particularly with another hard deadline from President Trump looming and the ongoing uncertainty around the reopening of the Strait of Hormuz. Alongside this, attention will begin to shift back toward macro data and policy signals, with the Fed’s March minutes, US CPI and other key releases offering the first real indication of how the energy shock is feeding through into inflation and activity.

At the same time, earnings season is now approaching and provides an important counterbalance to the geopolitical noise. Expectations remain relatively constructive, with the S&P 500 still on track to deliver a sixth consecutive quarter of double-digit earnings growth, led by strength in technology and energy, and supported by solid revenue momentum. Guidance has also been more positive than usual, suggesting that corporate America entered this period from a position of resilience. However, the concentration of that strength, combined with elevated oil prices and rising uncertainty, means markets will be closely watching for any signs that margins or demand are beginning to come under pressure.

If the geopolitical backdrop stabilises, earnings growth should return as the main driver of markets. Without a clear(er) off ramp and improvement in the inflation runway, the risk is that higher energy costs and tighter financial conditions will begin to erode this outlook rapidly.Top of Form

“…now this is not the end. It is not even the beginning of the end. But it is, perhaps, the end of the beginning…”

Now is not the moment for outsized bets – diversification, proper risk management and position sizing and ensuring the use of quality, adaptable investment managers is the key.

This content is intended for financial professionals only. These are the author’s views at the time of writing and may be subject to change. This content is not intended to provide the basis for any investment advice or recommendation. Any forecasts, figures, opinions, tools, strategies, data, or investment techniques are included for information purposes only.

The information presented is considered to be accurate at the time of production and has been obtained from or based upon sources believed by the author to be reliable and accurate, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Please visit our Regulatory Information and Terms of Use pages for more information.

Production

Production