Trump slapped by the Supreme Court; UK economic data firms

Author: Tom McGrath, CIO, 8AM Global Ltd

Last week was notable less for where markets finished and more for what they absorbed. Despite a landmark Supreme Court ruling reshaping US trade policy, softer US growth data and renewed geopolitical tension, global equities ended broadly steady.

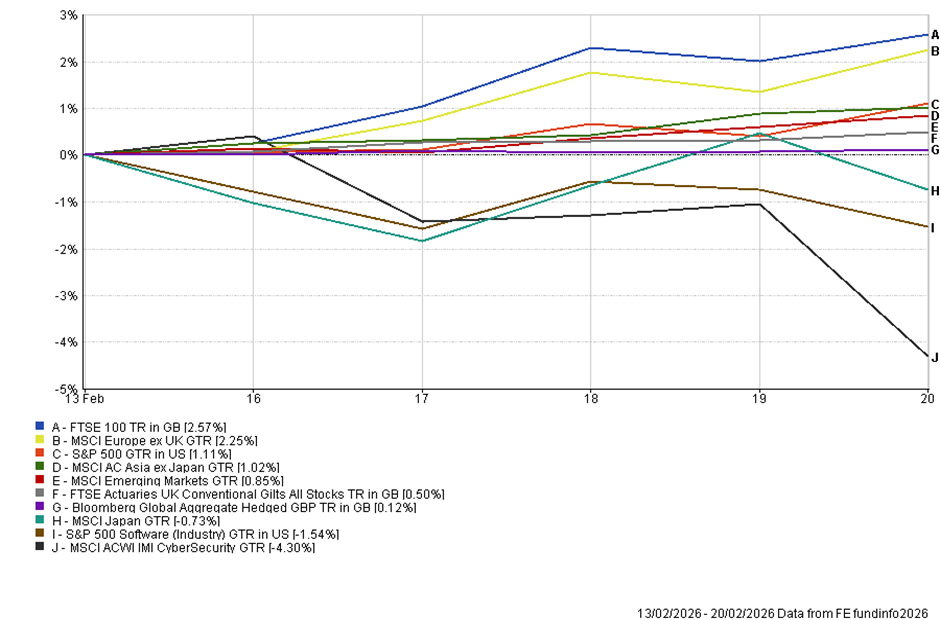

The UK led major markets, with the FTSE 100 rising roughly 2.7% in sterling terms. Europe gained around 2.3%, while the S&P 500 finished modestly higher at just over 1%. Emerging markets also edged into positive territory. Beneath the surface, dispersion widened, with software and cybersecurity stocks underperforming sharply, while value- and income-oriented indices proved more resilient.

Markets, in short, digested a potentially destabilising week with composure. That composure rests on a delicate balance: policy recalibration, slowing but still positive growth, and the assumption that inflation pressures remain contained.

US real GDP expanded at an annualised 1.4%, below expectations and down from 4.4% in the prior quarter. On the surface, the deceleration appears material. However, context matters. The government shutdown lasted for much of the quarter, with federal services curtailed and non-defence government spending falling at the sharpest pace since 2020. The Bureau of Economic Analysis estimates that the shutdown alone subtracted roughly one percentage point from growth.

Stripping out that distortion, the underlying activity appears closer to 2.4–2.5%. Consumer spending slowed to a still-solid 2.4% pace, business investment rose 3.7% — driven primarily by AI-related information processing equipment — and final sales to private domestic purchasers remained firm at 2.4%.

The composition of growth is telling. AI infrastructure spending continues to provide a significant offset to softer areas of the economy. Four major US technology firms are expected to collectively invest approximately $650 billion in data centre and related capital expenditures in 2026. That remains a powerful support for activity.

At the same time, there are clear signs of fragility. Excluding computer equipment and software, business investment has contracted for three consecutive quarters. Consumer sentiment remains subdued. Hiring has been historically weak outside recessionary periods, and the 2025 labour market performance was the softest non-recession year since 2003.

U.S. inflation data was also marginally firmer. Core PCE rose 0.4% month-on-month in December and is running at 3% year-on-year. That leaves the Federal Reserve in a holding pattern. Policy makers are reluctant to ease further while inflation remains above target. Yet, they must also monitor whether shutdown effects and trade uncertainty weigh more heavily on activity in the coming quarters.

The overall message is nuanced. Growth cooled, but not catastrophically. Underlying demand remains intact, supported by the consumer and AI-linked capital expenditure. The expansion continues, though at a more measured pace.

Trade policy: constrained but not abandoned

The Supreme Court’s 6–3 ruling striking down the bulk of President Trump’s tariff regime was the week’s political focal point. The decision removes the administration’s ability to rely on emergency powers under IEEPA to impose sweeping duties and forces a shift towards more procedural trade tools such as Sections 122, 301 and 232.

The White House responded quickly with a temporary 10% baseline levy, subsequently raised to 15%, and signalled further investigations into sectoral tariffs.

However, the ruling sends a clear signal that helps reaffirm the rule of law in the US and highlights that future measures will require more defined processes and are likely to be narrower in application. The decision also opens the door to potentially significant refunds for importers, introducing a near-term fiscal impulse alongside administrative complexity.

Politically, the timing is delicate. Polling indicates tariffs are associated with higher household costs, and with midterm elections approaching, the administration faces a balancing act between maintaining an ‘America First’ stance and avoiding further affordability pressure. The ruling may therefore result in a recalibration rather than an escalation.

Markets interpreted the development as reducing the probability of abrupt, large-scale trade expansion. Equities advanced modestly following the decision, and although bond yields headed higher, the moves were orderly.

United Kingdom: firmer data, improved fiscal optics

In contrast to US political turbulence, the UK finally delivered a series of positive economic surprises. January recorded the largest monthly budget surplus on record, with revenues exceeding spending by £30.4 billion, significantly above forecasts. Borrowing is running below both year-earlier levels and prior projections. Ten-year gilt yields have eased materially compared with a year ago, supporting debt-interest dynamics.

Retail sales reached a 20-month high, and the February flash composite PMI rose to 53.9, the strongest reading since April 2024. Private-sector activity has returned to solid expansion, defying earlier fears that substantial post-election tax increases would precipitate a downturn.

There are caveats. Part of the fiscal improvement reflects one-off capital gains effects. Unemployment has risen to a five-year high, and consensus still expects relatively modest growth in 2026. Nonetheless, the data flow has been materially stronger than anticipated.

For markets, the UK’s valuation profile and sector composition — less exposed to the most crowded AI themes and more geared towards income and real assets — have provided resilience during bouts of US-centric volatility.

Europe: incremental improvement

Europe also showed modest improvement. The composite PMI rose to 51.9, beating expectations and remaining in expansionary territory. Germany’s manufacturing sector expanded for the first time in more than three years, supported by increased defence and infrastructure spending.

While overall growth remains modest and risks from US trade policy persist, the direction of travel is constructive. The European Central Bank appears content to hold policy steady, with inflation broadly aligned to its 2% objective.

Sector rotation: AI disruption debate intensifies

Late in the week, renewed concern emerged around AI’s disruptive reach, particularly following reports of new cybersecurity tools. Cyber and software names underperformed sharply. While AI will undoubtedly reshape workflows and competitive dynamics, the sell-off appeared indiscriminate. Cybersecurity remains mission-critical, deeply embedded and subject to regulatory and reputational constraints. AI is more likely to augment leading platforms than replace them outright.

The episode illustrates a broader theme: markets are increasingly sensitive to AI-related competitive risk. That sensitivity is likely to produce further volatility.

Looking ahead

Attention now turns to Nvidia’s results, which will be central to the sustainability of the AI capex narrative. Investors will focus on demand visibility, margin resilience and evidence that infrastructure investment is translating into durable revenue streams.

Trade policy developments will remain fluid, but the Supreme Court’s ruling has introduced procedural friction that may temper the pace of escalation. On the macro front, the key question is whether the recent cooling in growth proves temporary or signals a more persistent moderation.

For now, markets are navigating policy noise with relative composure. The expansion continues, albeit at a slower pace, and earnings breadth outside the narrow AI complex is gradually improving. The balance remains delicate, but it is not yet breaking.

This content is intended for financial professionals only. These are the author’s views at the time of writing and may be subject to change. This content is not intended to provide the basis for any investment advice or recommendation. Any forecasts, figures, opinions, tools, strategies, data, or investment techniques are included for information purposes only.

The information presented is considered to be accurate at the time of production and has been obtained from or based upon sources believed by the author to be reliable and accurate, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Please visit our Regulatory Information and Terms of Use pages for more information.

Production

Production