Trump backs down on Greenland; UK data firms sterling

Author: Tom McGrath, CIO, 8AM Global Ltd

The week began with an uncomfortable reminder that geopolitics can still intrude abruptly into markets accustomed to policy support and economic resilience. President Trump’s renewed rhetoric around Greenland, combined with the threat of tariffs should other nations resist US ambitions, triggered an early bout of risk aversion. The reaction was less about the specifics of Greenland itself and more about what it symbolised: a willingness to use trade and economic pressure as a geopolitical tool, at a time when markets remain sensitive to anything that could reintroduce inflation risk or disrupt global supply chains.

That initial shock faded as the week progressed. By the time leaders convened at Davos, the tone had softened, with talk shifting towards frameworks and dialogue rather than confrontation. Markets took this as a signal that the worst-case outcomes were unlikely in the near term, and much of the early-week volatility was retraced. This pattern has become familiar. Political noise still matters, but unless it escalates into something concrete and sustained, investors are increasingly inclined to look through it and refocus on growth, earnings and policy.

US

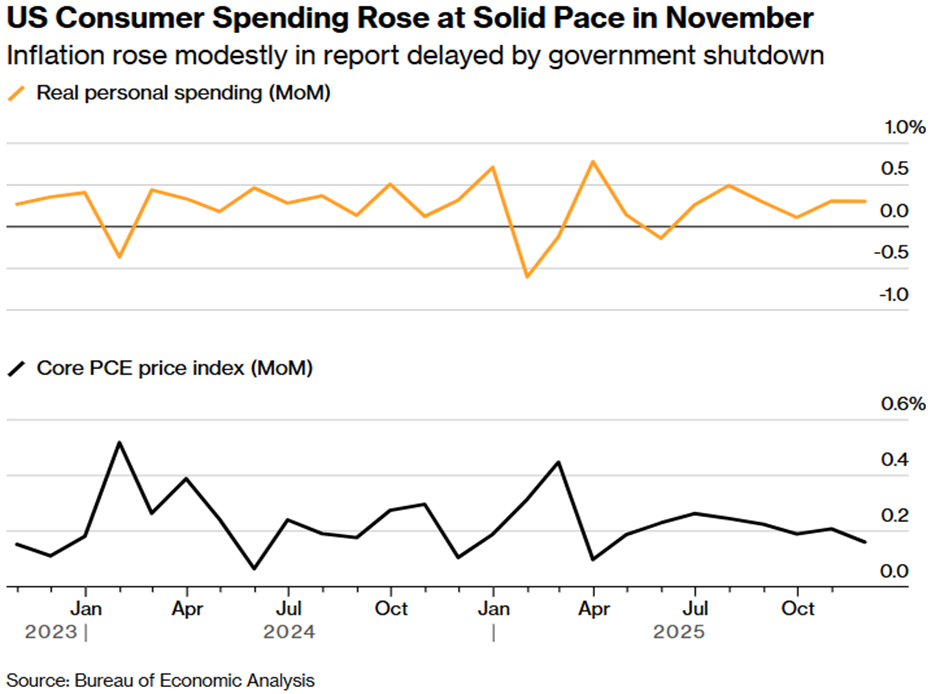

Underneath the geopolitical headlines, the more important driver of markets last week was the reassessment of the interest rate outlook, particularly in the United States. A run of economic data reinforced the view that the US economy remains resilient, even after a period of aggressive monetary tightening. Jobless claims remained low, suggesting limited layoffs, while consumer spending rose at a solid pace, supported by rising nominal wages. Together, these data points strengthened the argument that the Fed does not need to rush back into easing.

This was reflected clearly in bond markets. Short-dated US Treasury yields moved higher as investors pushed out expectations for the next rate cut, with the two-year yield reaching its highest level since December. Longer-dated yields, however, were more subdued, leaving the curve flatter rather than dramatically steeper. The message from the bond market was nuanced rather than alarmist. Growth looks firm enough to delay cuts, but inflation does not appear to be re-accelerating in a way that would force policy back into restrictive territory.

The Fed’s preferred inflation measure, Core PCE inflation, remains sticky but stable, hovering just below 3% year on year. Complicating interpretation is the lingering distortion from last year’s government shutdown. Policymakers are well aware of these limitations, and the prevailing view remains that the upcoming Federal Reserve meeting will keep rates steady, with guidance emphasising patience rather than urgency.

Market pricing reflects this stance. Futures imply little chance of a move at the January meeting, with expectations centred on one cut by mid-year and possibly a second by the end of 2026. That profile represents a meaningful shift from the more aggressive easing assumptions that prevailed late last year. However, it is still consistent with a benign macro backdrop rather than a policy mistake. In effect, investors are accepting that ‘higher for longer’ may mean ‘later than hoped’, not ‘forever’.

UK

The economic data during the week was more constructive than feared. Retail sales recovered in December, rising modestly after two consecutive monthly declines. The strength was concentrated online, with jewellery and food sales standing out, suggesting consumers remain willing to spend selectively even if confidence is fragile. The data provided some reassurance that household demand has not rolled over entirely, though the broader picture remains one of cautious spending behaviour rather than a full-blown revival. Public finances/tax receipts also came in stronger, with December central government current receipts up meaningfully year-on-year and tax receipts higher (including income tax, corporation tax and VAT). Reasons enough for the Pound to end the week up strongly versus the USD.

Europe

Elsewhere in this neck of the woods, the macro backdrop remains steady but unexciting. Flash PMI data suggested ongoing (modest) expansion, but the pace wasn’t quite as strong as hoped, steady rather than accelerating. That’s consistent with European equities lagging on the week: not a crisis, just a lack of catalysts versus the US. For now, Europe is benefiting from global stability rather than driving it, leaving markets there more dependent on external catalysts than on domestic momentum.

Asia

Attention turned to Japan, where political developments unsettled markets early in the week. Comments around fiscal policy, including proposals to suspend food taxes, reignited concerns about Japan’s already substantial public debt burden. This added pressure to Japanese government bonds and the yen. The BoJ’s latest outlook reiterates a moderate growth baseline supported by policy and a virtuous income-to-spending cycle, while acknowledging external policy/trade uncertainty. We, and as far as we can tell, everyone else, remains convinced by the long-term story in Japan but finds little reason to add to any position over the shorter term.

China

The picture remains mixed. Policy support continues to underpin growth, and headline data has stabilised, but confidence is still uneven and sensitive to global trade dynamics. China benefits from easing global financial conditions yet remains exposed to any deterioration in the external environment. No news isn’t good news – it’s just no news!

Market Breadth

One of the more encouraging features of 2026 remains the gradual broadening beneath the surface. While US mega-cap technology continues to matter, leadership is no longer as narrow as it was through much of last year. Smaller companies, materials and selective cyclicals have begun to participate more consistently, a pattern that typically aligns with an economy that is maturing. Valuations in parts of the market are clearly full, but they are being supported by real earnings delivery rather than pure multiple expansion.

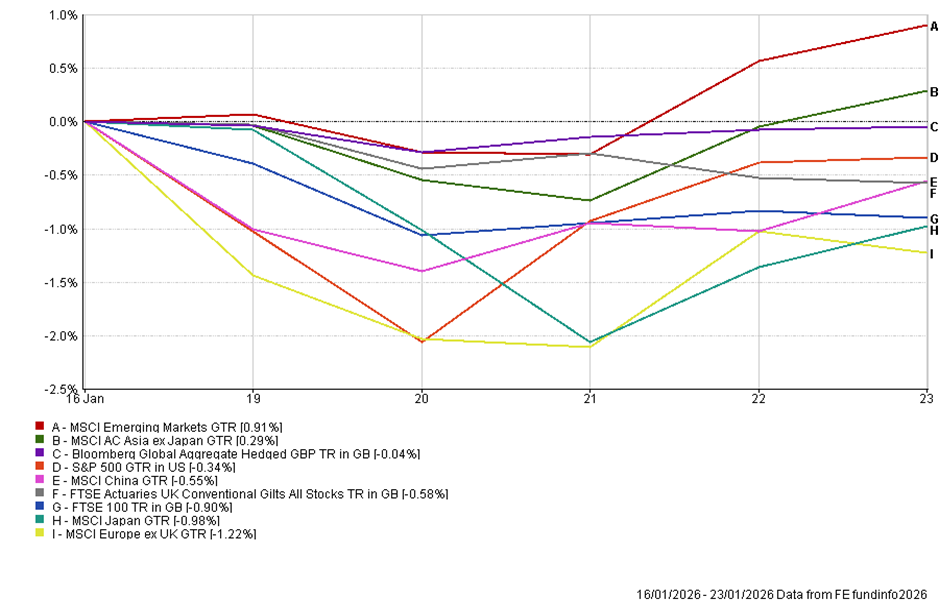

Earnings news added useful texture rather than a single dominant theme. Results from companies such as Netflix reinforced the importance of scale, pricing power and disciplined execution in a more mature growth environment. Upbeat commentary from Nvidia continued to underpin confidence that AI-related capital spending remains intact, even as investors become more selective about where the returns from that spending ultimately accrue. This is consistent with a broader shift away from indiscriminate ‘AI adjacency’ toward a more discriminating focus on balance sheets, margins, and end demand. The strength in Emerging Markets also suggests that investors are looking elsewhere for returns this year.

This week

The immediate focus will be on central banks and earnings. The Fed meeting next week is unlikely to deliver a policy change, but the language around patience versus progress will matter for bond yields and equity multiples. Meanwhile, the next phase of earnings will test whether the recent broadening in equity leadership can be sustained or whether investors retreat once again to perceived defensives.

Sentiment is the final piece of the puzzle. Optimism has clearly risen, and that in itself creates the conditions for short-term corrections. From a contrarian perspective, too much good news can be its own risk. That said, periods of elevated sentiment during earnings-driven expansions have often coincided with further upside rather than imminent collapse. This still feels like a year where volatility will be frequent, headlines will be unsettling, but the underlying forces supporting growth and profits remain firmly in place.

This content is intended for financial professionals only. These are the author’s views at the time of writing and may be subject to change. This content is not intended to provide the basis for any investment advice or recommendation. Any forecasts, figures, opinions, tools, strategies, data, or investment techniques are included for information purposes only.

The information presented is considered to be accurate at the time of production and has been obtained from or based upon sources believed by the author to be reliable and accurate, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Please visit our Regulatory Information and Terms of Use pages for more information.

Production

Production