Geopolitics returns to the foreground

Author: Tom McGrath, CIO, 8AM Global Ltd

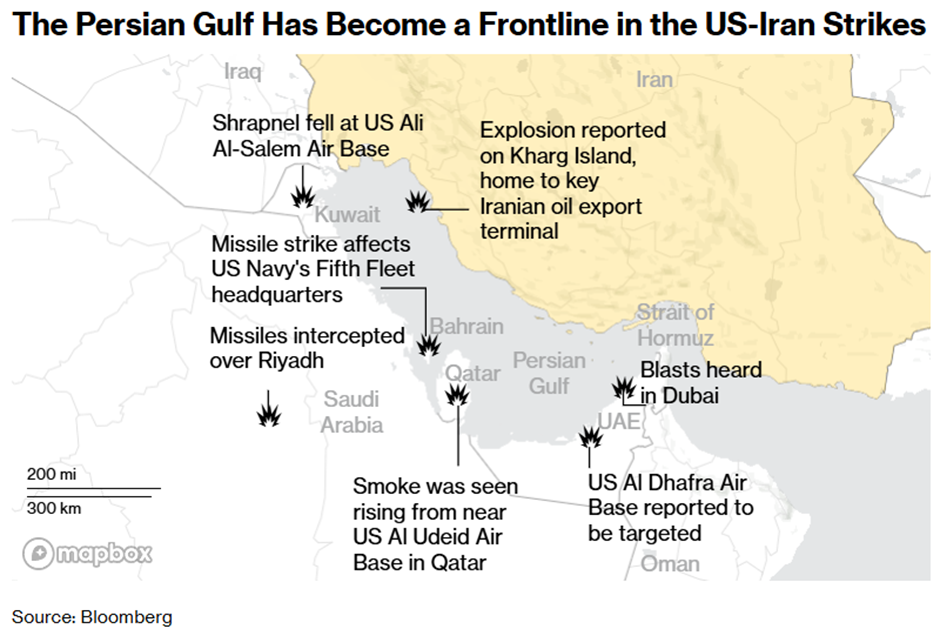

Markets move into the new week facing a material geopolitical shift following the coordinated US–Israeli strikes on Iran and the death of Supreme Leader Ayatollah Ali Khamenei. Iran’s subsequent retaliation across parts of the Gulf region has widened the confrontation and introduced a degree of strategic uncertainty that markets had not been pricing. The death of a figure who has defined Iran’s political and religious structure for decades is not merely a military development but a constitutional and institutional shock. A temporary leadership council has been announced, yet the succession process within the Islamic Republic remains opaque, and that opacity inevitably increases risk premia across the region.

Financial markets are typically less concerned with political symbolism than with economic transmission channels. The immediate focus is therefore on energy flows, shipping routes and regional infrastructure. Iran’s geographic position alongside the Strait of Hormuz gives it disproportionate influence over global oil markets. Roughly a fifth of internationally traded crude passes through that corridor, and even limited disruption can move prices meaningfully. Reports of shipping hesitation and rerouting activity are sufficient to introduce a geopolitical premium into crude, regardless of whether physical infrastructure has yet been damaged.

It is important to separate structural disruption from headline volatility. In previous episodes of regional escalation, oil prices have spiked quickly and then retraced once it became clear that production and export facilities were largely intact. The durability of any move higher will depend on physical constraints rather than rhetoric. OPEC+ retains spare capacity, and recent commentary has suggested a willingness among key producers to adjust supply should instability threaten broader balance. The path of crude over the coming week will therefore be a more important signal than the opening gap.

A complication for inflation…

The geopolitical escalation arrives at an awkward moment for inflation dynamics. US Producer Price Index data released on Friday came in firmer than expected, nudging bond yields higher and tempering confidence in imminent policy easing. While the data did not fundamentally alter the disinflation trend that has been underway for some time, it did remind investors that progress is uneven and that upstream price pressures have not entirely disappeared.

An energy-driven rise in crude would feed mechanically into headline inflation measures over the coming months. Central banks may choose to look through such moves if they are judged transitory, but markets tend to react more immediately. The interaction between oil and bond yields will therefore be central. If yields remain relatively contained despite firmer energy prices, it would suggest confidence that the broader inflation trajectory remains intact. A sustained rise in yields would imply that markets are reassessing the rate path more meaningfully.

NVIDIA and a changing tone in ‘Technology’

Against this macro backdrop, last week’s corporate focal point was NVIDIA’s earnings release. Operationally, the results were strong. Revenue growth remained robust, forward guidance pointed to continued hyperscaler demand, and there was little indication of a retrenchment in capital expenditure for AI infrastructure. By historical standards, the numbers would have been considered unequivocally positive.

The more interesting development was the market reaction. The share price softened despite the strength of the print, underscoring a shift in investor psychology. The earlier phase of the AI rally was characterised by multiple expansions driven by optimism around transformative potential. That phase has now transitioned to one in which investors are scrutinising capital intensity, the sustainability of margins, and the translation of growth into free cash flow. The sell-off was not a repudiation of the AI theme but rather evidence that expectations had already moved ahead of realised delivery.

This dynamic partly explains why the US market has struggled to make decisive gains in February despite broadly resilient earnings. The concentration of index leadership in a handful of large technology names leaves the broader market sensitive to valuation recalibration within that fairly sizeable chunk.

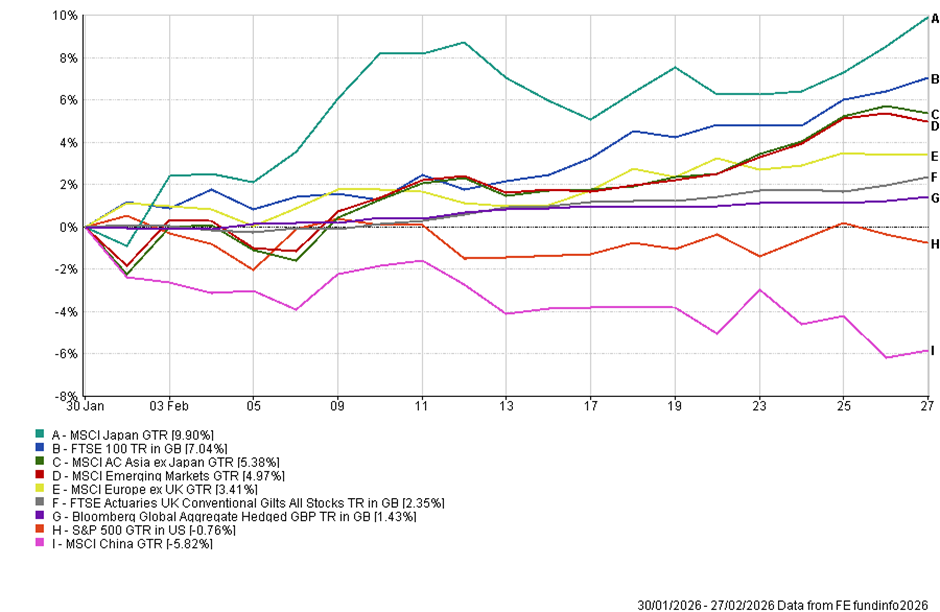

February performance: divergence and rotation

The February index performance data illustrates a notable divergence across regions. Japan has delivered the strongest returns among major developed markets, reflecting a combination of corporate reform momentum, currency dynamics and relatively attractive valuations. The FTSE 100 has also performed well, supported by its heavy weighting in energy and mining companies, both of which benefit in environments where commodity prices firm.

Asia ex Japan and Emerging Markets have posted solid gains, suggesting that capital has not been confined to US equities. In contrast, the S&P 500 has largely moved sideways over the month, digesting elevated valuations and mixed inflation signals. China has underperformed, continuing to grapple with domestic structural challenges and uneven confidence.

Markets with greater exposure to real assets and cyclical commodities have outperformed those dominated by long-duration growth. This pattern suggests a broadening of leadership rather than a wholesale deterioration in global risk appetite. That shift has been incremental, but it is visible in the dispersion of returns.

This week…

The immediate opening tone will likely be shaped by energy pricing and safe-haven flows. However, the more consequential developments will unfold in the days that follow. Markets will be assessing whether oil stabilises after the initial reaction, whether bond yields remain anchored despite geopolitical stress, and whether equity weakness is concentrated or broad-based.

The global economy, as it stands, is not displaying clear recessionary characteristics. Corporate earnings outside a narrow set of high-valuation sectors remain broadly constructive. Inflation has moderated from its prior peaks, even if the final leg of disinflation proves more complex. What the current episode does is reintroduce volatility into a market that had been moving toward greater complacency.

Ultimately, geopolitical events tend to affect asset prices through an identifiable economic signal rather than solely through emotion. Energy supply, shipping routes and inflation expectations will determine whether this episode remains a short-lived shock or evolves into a more persistent macro headwind. Those variables will matter more than the initial headlines and inevitable short-term market volatility.

This content is intended for financial professionals only. These are the author’s views at the time of writing and may be subject to change. This content is not intended to provide the basis for any investment advice or recommendation. Any forecasts, figures, opinions, tools, strategies, data, or investment techniques are included for information purposes only.

The information presented is considered to be accurate at the time of production and has been obtained from or based upon sources believed by the author to be reliable and accurate, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Please visit our Regulatory Information and Terms of Use pages for more information.

Production

Production