The return of the geopolitical risk premium as the war escalates

Author: Tom McGrath, CIO, 8AM Global Ltd

The ongoing conflict between Iran, the United States and Israel intensified over the weekend as the war entered its ninth day, with both sides widening their targets and signalling that the fighting could persist for some time. Iran confirmed that it has selected a new Supreme Leader following the death of Ayatollah Ali Khamenei at the start of the conflict. However, the identity of the successor has not yet been publicly disclosed (at the time of writing).

Update: 15:17:00 – Mojtaba Khamenei has been named as successor to his father.

At the same time, the military confrontation escalated further. Iranian forces struck a water desalination facility in Bahrain while Israel launched fresh attacks on major fuel depots in Tehran and warned that Iranian power infrastructure could become a target. Gulf states, including the United Arab Emirates, Kuwait, Saudi Arabia and Bahrain, reported intercepting further Iranian missile and drone attacks overnight, highlighting how widely the conflict has now spread across the region.

Iranian officials have stated that the country has the capacity to sustain the war for months (albeit at a lower cadence given limited missile stocks) and warned neighbouring states that any territory used as a base for US operations may be treated as a legitimate target.

Meanwhile, Israel has continued efforts to degrade Iran’s military capabilities, claiming to have destroyed a significant proportion of its missile launch infrastructure while striking energy and logistics assets inside the country. The situation has already begun to affect regional energy production and shipping routes. The UAE and Kuwait have both reduced oil output amid the near-closure of the Strait of Hormuz, the narrow waterway through which roughly a fifth of global energy exports normally pass.

President Trump has indicated that the US may consider widening its strikes if necessary, while suggesting the conflict could continue “for a little while” before oil markets eventually stabilise.

Against this backdrop, it is no surprise that markets were forced to reprice geopolitical risk quickly. For much of this year, investors had been focused on a relatively familiar set of drivers: the pace of US growth, the path of inflation, the likelihood of interest rate cuts and the continuing enthusiasm around artificial intelligence and large-cap technology. Last week, those themes were pushed firmly into the background. The escalation of this conflict and the resulting surge in energy prices have brought geopolitical risk back to the centre of the investment narrative.

Energy markets themselves were the clearest transmission channel. Brent crude moved above $92 a barrel while US crude finished the week above $90, marking the largest weekly percentage increase in US oil prices since the 1980s and futures suggest we may be heading over $100 on Monday morning.

Update: 15:17:00 – Oil hit $119.50 a barrel today.

The move reflects growing disruption across the Gulf region, particularly around the Strait of Hormuz. Even without a formal closure, insurance withdrawals, military activity and shipping delays have severely restricted tanker traffic. Traders estimate that as much as 7–11 million barrels per day of supply could be temporarily affected if disruptions continue, forcing markets to price a much tighter near-term energy balance.

The performance across asset markets last week reflected exactly this dynamic as most global equity markets fell between roughly 5-6%. European equities, Japan and emerging markets were among the weakest performers, while the US held up somewhat better. Gold rose modestly, and fixed income also sold off as inflationary worries grew. Importantly, however, markets are not yet behaving as though the global financial system is under severe stress. What we are seeing so far looks more like a repricing of geopolitical risk rather than a full-scale financial shock.

The relative resilience of the US market also makes sense in this context. The United States is far less vulnerable to external energy supply disruptions than Europe or many Asian economies due to its large domestic energy production. By contrast, Europe remains particularly exposed to higher imported energy costs, especially given the ongoing fragility in global gas markets and LNG supply routes. In periods of geopolitical uncertainty, global capital also tends to flow toward the US rather than away from it, providing some resilience for US assets.

US economic data

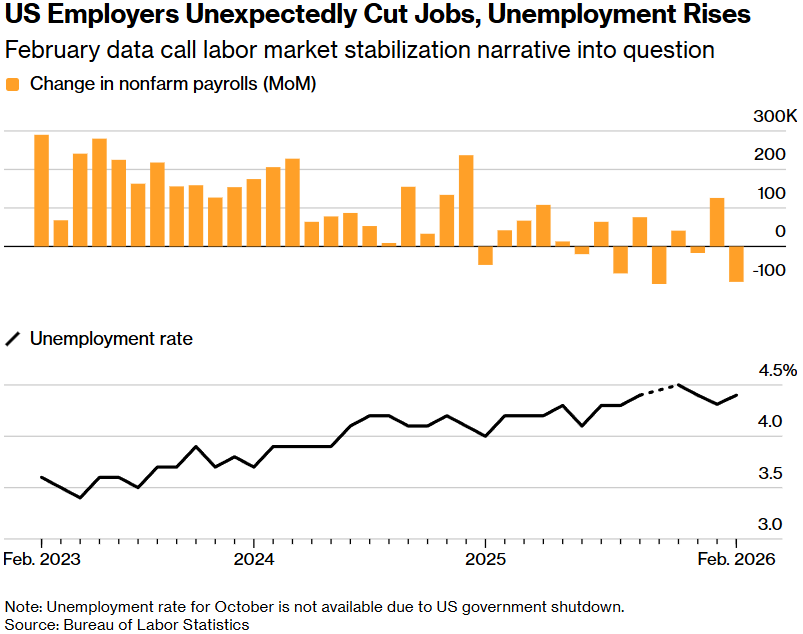

Alongside the geopolitical developments, last week also delivered an awkward set of US economic data. February’s non-farm payrolls report showed a decline of 92,000 jobs, one of the largest monthly drops since the pandemic and well below expectations for modest growth. The unemployment rate rose to 4.4% while retail sales also disappointed.

Under normal circumstances, such data would strengthen expectations that the Federal Reserve may begin cutting interest rates later this year. Instead, the report raised a more uncomfortable question about whether the labour market is becoming more fragile than many had assumed.

Temporary factors, including poor weather and strikes in the healthcare sector, can explain some of the weakness. However, the breadth of job losses across industries suggests that hiring momentum may genuinely be slowing. Several sectors, including manufacturing, transport and information services, reported job cuts. At the same time, productivity gains and increasing investment in artificial intelligence are allowing some firms to operate with leaner staffing levels. In other words, the labour market may not be deteriorating sharply, but it is cooling more noticeably than recent data had suggested.

Unfortunately for policymakers, the report was not entirely benign from an inflation perspective. Average hourly earnings rose 0.4% on the month, indicating that wage pressures remain present. In addition, the surge in oil prices complicates the calculation. US gasoline prices have already risen sharply and could climb further if energy disruptions persist. Weak growth combined with rising energy costs is exactly the type of combination that central banks find difficult to manage. A softer labour market (under normal circumstances) would open the door to rate cuts later in the year. Yet an energy-driven inflation impulse may delay that process or at least make policymakers more cautious about moving too quickly.

UK

Events in the Middle East largely overshadowed Rachel Reeves’ spring fiscal update, yet it still offered some insight into the domestic economic outlook. The Office for Budget Responsibility downgraded its forecast for UK growth in 2026 to 1.1% from 1.4% previously while still expecting inflation to ease toward 2.3% next year and return to the BoE’s 2% target by 2027. Reeves pointed to a slightly larger fiscal buffer than previously forecast, but the broader message was one of stability rather than new policy intervention. Importantly, the OBR also warned that its forecasts were prepared before the escalation in Iran and could quickly become outdated if energy prices remain elevated.

China

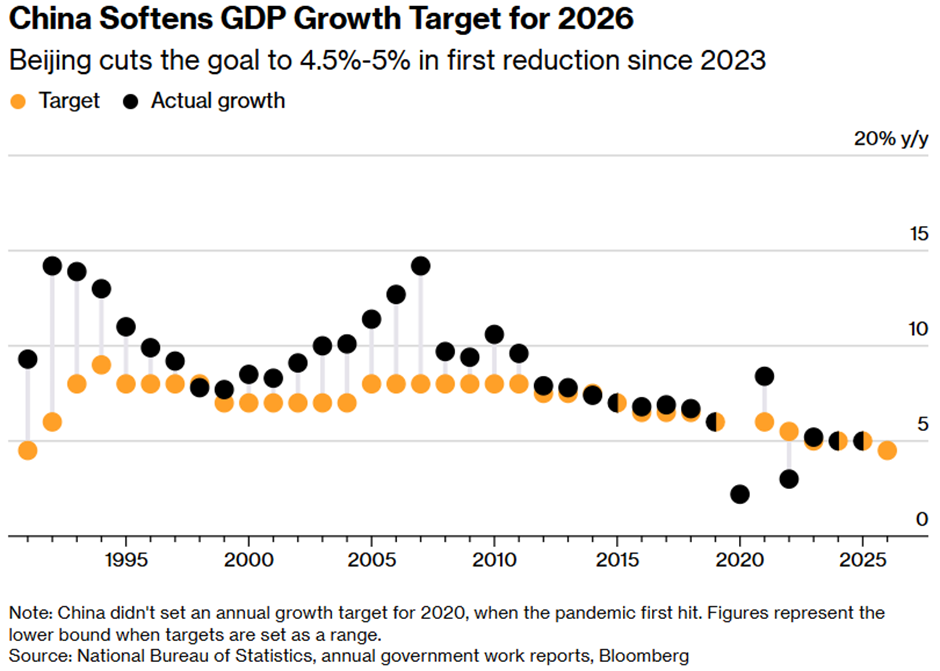

China offered a different form of realism. Beijing set its 2026 growth target at 4.5%-5%, the lowest since the early 1990s, and a clear acknowledgement that the model that powered China’s rapid economic expansion for decades is now under strain. Policymakers continue to emphasise technology development, industrial upgrading and artificial intelligence while offering only limited new measures to stimulate household consumption. The property sector remains weak, and consumer spending continues to lag behind most developed economies.

This Week…

The key question for markets now is whether the current developments represent a temporary shock or the beginning of something more persistent. Our inclination remains cautiously constructive, although with more humility than a week ago. Historically, most geopolitical shocks have not permanently derailed global equity markets. Energy spikes tend to fade once supply routes adjust and the true scale of disruptions becomes clearer. The US economy, while softening somewhat, is not entering recession, and corporate earnings have so far remained reasonably resilient.

At the same time, the longer the conflict drags on, the more uncomfortable the macro backdrop becomes. Oil approaching $100 a barrel would inevitably feed into inflation expectations and consumer confidence. Politically, it is also difficult to imagine that President Trump will tolerate sustained increases in gasoline prices without eventually searching for some form of diplomatic off-ramp. The incentives for de-escalation are therefore likely to grow over time, even if the path toward that outcome remains uncertain.

For now, markets are adjusting to a renewed geopolitical risk premium rather than panicking. The coming weeks will determine whether that premium fades as tensions ease or becomes a more persistent feature of the global economic landscape.

This content is intended for financial professionals only. These are the author’s views at the time of writing and may be subject to change. This content is not intended to provide the basis for any investment advice or recommendation. Any forecasts, figures, opinions, tools, strategies, data, or investment techniques are included for information purposes only.

The information presented is considered to be accurate at the time of production and has been obtained from or based upon sources believed by the author to be reliable and accurate, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Please visit our Regulatory Information and Terms of Use pages for more information.

Production

Production